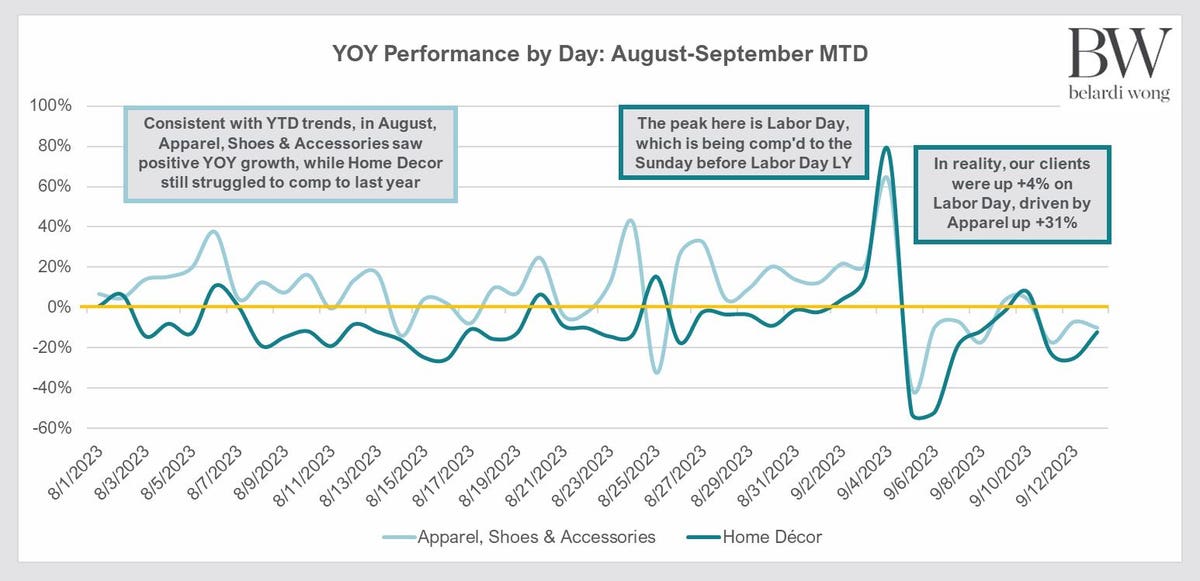

The New Belardi Wong performance report is indicative of modest sales gains by DTC companies. The study reports softer sales in August than in July when Prime Day was a positive factor. The survey sees a 1% decline for all industries. However, apparel companies show a 13% year-over-year increase in August with strength ahead of Labor Day. September revenues are down 6% in all industries however apparel is up a mild 4%

It is probable that back-to-school apparel purchases helped the increases in apparel. DTC sales during the Labor Day weekend were strong (+25%) in apparel. DTC sales were also strong during the 2022 Labor Day which also increased +25%. Steve Sadove, former Saks Fifth Avenue chairman and CEO, spoke recently at Wells Fargo conference and said that “restrained markdowns and carefully controlled inventories led to “okay” back-to-school sales.

With this in mind, it is hard to see a quick turn-around of consumer spending. Gasoline prices have risen to around $6.00 in California, food prices are still high and apparel is still higher than expected. It is likely that retailers are planning a strong promotional attack for the Holiday selling period, which is likely to start as early as October and last until December 24.

Early sales forecasts for the Christmas season are very modest since inflation seems to be stagnating and the buying power of the consumer is eroding. As we veer into the holiday selling season, the forecasts have shifted to less consumer buying power.

1. Deloitte Forecast sees holiday retail sales increase between 3.5% and 4.6% with an overall projected sales totaling $1.54 to $1.56 trillion during the November to January timeframe.

2. Retail sales between November 2022 and January 2023 (seasonally adjusted and excluding automotive and gasoline) grew 7.6% and totaled $1.49 trillion according to the U.S. Census Bureau.

3. Deloitte sees E-commerce sales to grow 10.3% to 12.8% year-over-year, totaling between $278 billion and $284 Billion this season. This compared to 7.9% growth last year with a $252 billion total spend.

4. Bain & Co. forecasts unadjusted seasonal sales growing 3.0 percent year-over-year in November and December to nearly $915 billion. This forecast suggests the slowest growth since 2018. Bain projects a 90% growth for non-store sales and real U.S. holiday sales growth will be sluggish at just 1.0% well below the 10-year average and the lowest real sales growth since the financial crisis in 2008.

POSTSCRIPT: During July and August there were 17 states that had tax-free weekends for back-to-school shoppers. Most of the tax-free allowance was for apparel, some for computers. That was an incentive that few shoppers ignored. There will be no tax relief from now until Christmas. However, most retailers will have sales that will help consumers. Manufacturers are likely to produce orders, but do not plan for re-orders. Shoppers will be well advised to shop for gifts early; if they see something they like, they should buy right away, it may not be available later on.

Read the full article here