By Ewa Manthey

Gold surges on safe-haven bets

Gold dropped to a low of around $1,810/oz on 4 October after the release of strong US jobs data fueled expectations for a further US rate hike before the end of the year. Then, the direction of gold prices quickly changed following the outbreak of Israel-Hamas conflict on 7 October, with the precious metal nearing its record of about $2,075/oz set in 2020. Gold rallied 7.3% last month as demand for safe-haven assets has increased. We believe gold is likely to continue to benefit if Middle East tensions increase.

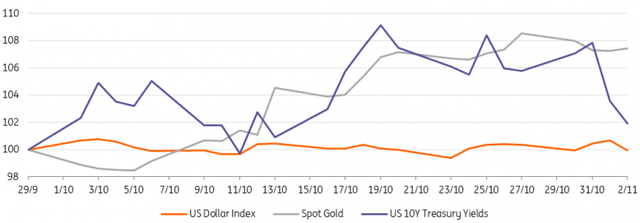

Safe-haven demand outweighs rising bond yields, US dollar

Refinitiv Eikon, ING Research

Demand for safer assets has outweighed the impact of rising real yields, which are normally a key driver of non-interest-bearing precious metal. Since the onset of the Israel-Hamas conflict, real yields rose 7.7% month over month, reaching a new high since 2007 while the US dollar trade-weighted index rose to an 11-month high in October. Higher yields and a stronger dollar are typically negative for gold. However, the precious metal has held up well despite its surge, with geopolitical tensions becoming a bigger factor.

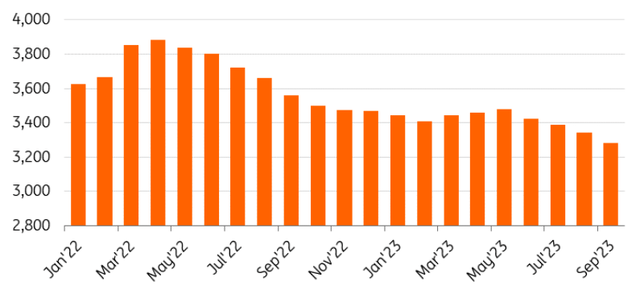

Gold ETFs see ongoing outflows

Yet, total holdings in bullion-backed ETFs have continued to decline despite rising spot prices. Gold ETFs have seen outflows of 189 tonnes so far this year and have now registered six successive quarters of negative demand, data from the World Gold Council (WGC) showed, with ETF and futures investors showing little appetite for the precious metal with rising bond yields offering an alternative source of real income for investors. Holdings fell by 139 tonnes (-US$8bn), although this was an improvement on the 244-tonnes outflow in the second quarter of 2022. Over the first nine months of this year investment demand was down by 21%, with most of that weakness driven by ETFs, particularly in the US and Europe, as investors increasingly took the view that major central banks – particularly the US Fed – will keep rates higher for longer.

ETF outflows continue

World Gold Council, ING Research

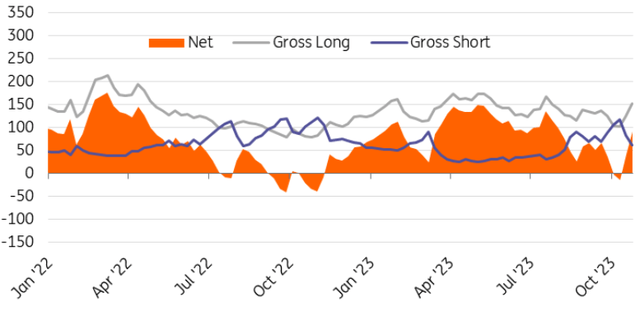

However, net-long positioning, reflecting sentiment in the gold market, turned positive in the second half of October as spot prices surged. COMEX net-long positionings rose 137% month over month to 29 October.

Investors fly back to safe-haven assets

CFTC, WGC, ING Research

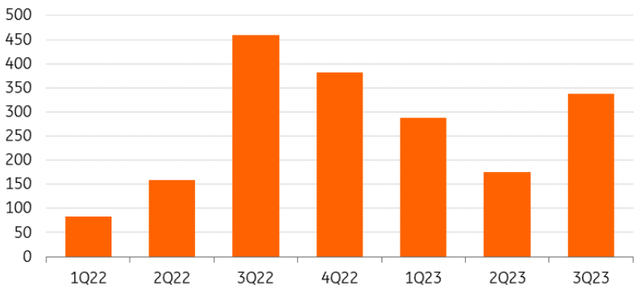

Central banks demand hits year-to-date record

Central banks have purchased around 800 tonnes of gold over the first three quarters of 2023, according to data from the World Gold Council (WGC). This was a record amount bought for a nine-month total, as geopolitical concerns pushed central banks to increase allocation towards safety assets. Central banks’ healthy appetite for gold is also driven by countries’ desire to weaken their dependence on the US dollar as a reserve currency.

Central banks increased their gold purchases to 337t over the third quarter of the year, primarily due to higher buying from China (+78 tonnes), Poland (+57 tonnes), Turkey (+39 tonnes) and India (+9 tonnes). China has been the largest buyer of gold this year amid an 11-month buying streak. The People’s Bank of China has purchased 181 tonnes this year, taking gold holdings to 4% of its reserves.

Year-to-date, central bank net buying of gold is 14% ahead of 2022. This insatiable appetite has helped gold prices defy surging bond yields and a strong dollar. We believe this trend is likely to continue in the fourth quarter amid tensions in the Middle East.

China leads central banks’ gold buying spree

World Gold Council, ING Research

Fed nearing the end of its tightening rate cycle

The Fed held rates steady in November, for a second straight meeting, as was widely anticipated. However, Fed Chair Jerome Powell hinted the bank may be done with further tightening. In latest US data, non-farm payrolls rose 150,000 in October, below the estimate, and the unemployment rate unexpectedly rose, taking the pressure off the Fed to tighten policy further. Payrolls is the number that markets focus on and with unemployment rates and wages softening it all reinforces the view that the Fed is finished hiking interest rates, as our US economist believes.

Lower rates are typically positive for gold, which doesn’t offer any interest.

Our US economist believes that the need for further policy rate hikes is now dramatically reduced and expects the starting point for Fed rate cuts in the second quarter of 2024.

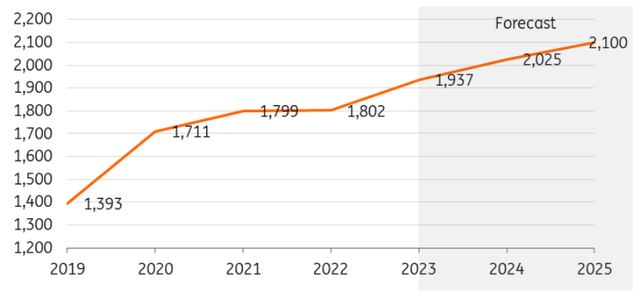

Gold eyes more gains

We have revised our fourth quarter forecast upwards to $1,950/oz, raising our 2023 average to $1,937/oz given the outbreak of the Israel-Hamas conflict and the risk of tensions escalating in the Middle East. However, we still believe the Fed’s higher-for-longer narrative will keep the rally in check.

Looking into next year, we expect gold prices to move higher again next year to average $2,025/oz on the assumption that the Fed starts cutting rates in the second quarter of next year, the dollar weakens, safe-haven demand continues amid global economic uncertainty and central bank buying remains at high levels.

ING forecast

ING Research

Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Original Post

Read the full article here