By Robert Carnell

Nothing to see here

Let’s be very clear about what deflation is and what it isn’t. It is a very pernicious situation, where the “general price level” which includes consumer prices, but also other prices such as real and financial assets and money wages decline. And it leads to a sharp slowdown in economic activity as it deters consumer spending and investment.

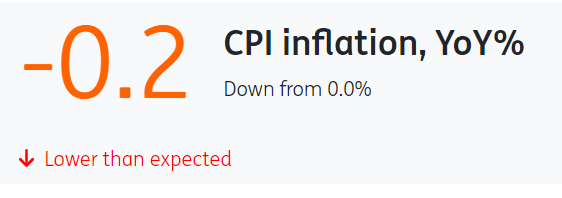

What China has right now is a low rate of underlying inflation, which reflects the fact that domestic demand is fairly weak. What today’s data show is that it doesn’t take much of a negative shock from one of the components to push a low underlying headline inflation rate below zero on a year-on-year basis.

If you want to use any term, “disinflation” would be my preference, but what we are seeing today is mainly the result of a supply excess, rather than a collapse in demand.

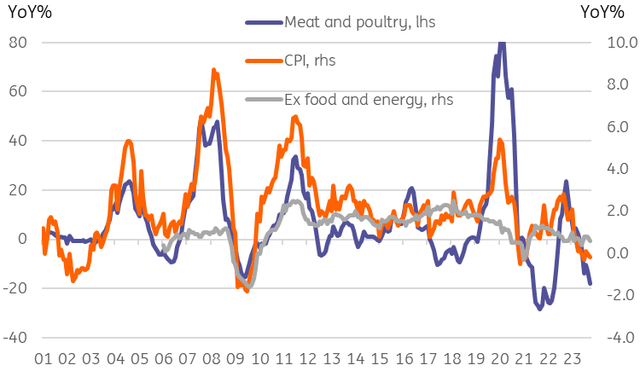

China’s headline and core inflation rates

CEIC, ING

Bring on Mordecai Ezekiel

In 1925 (says Wikipedia), the “Hog cycle” was first coined as a term in agricultural economics, by the colourfully named Mordecai Ezekiel. What he noted was that when pork prices were high, farmers kept back pigs from slaughter to build their herds, which ultimately led to a glut the following season and a collapse in prices which then led to herd shrinkage, which in turn pushed prices back up again, and so on…

It might be nearly 100 years old, but the hog cycle is alive and well in China.

In the chart above, you can see how meat and poultry prices in China rose in 2022 – another bout of swine fever taking its effect and shrinking herds. Prices for pork are now subsiding again as pork supply has increased, dragging the headline inflation rate down. Stripping out food and energy, inflation is currently 0.6% YoY, and down only very slightly over the last few months.

0.6% is still quite a low rate of inflation if we take this to be the underlying rate for China, and it is indeed a reflection of what is still a fairly weak backdrop for domestic demand.

Wholesale pork prices so far for November continue to fall, but the rate of decline appears to be easing as pork prices near their previous lows. So we may still see a negative drag from food and possibly energy next month (given what is happening to crude prices too), but the drag is likely to be smaller, and thereafter, absent further supply shocks, inflation is likely to start heading higher again.

What’s the story?

While negative headlines for Chinese CPI inflation provide the media with a hook to hang a juicy story on, the truth is considerably less tasty. Next week, we get further activity data for China. The most recent figures have shown very slight indications of firming, and we imagine that we will see something similar this time, notwithstanding the disappointing PMI data for October.

If so, then this would be a further set of data that would not be consistent with the deflation story being peddled in some corners, even if we concede that China’s macro condition remains fairly soft and vulnerable to negative shocks.

Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation, or investment objectives. The information does not constitute an investment recommendation, and nor is it investment, legal, or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Original Post

Read the full article here