Elevator Pitch

Trupanion, Inc. (NASDAQ:TRUP) shares are assigned a Hold investment rating. I have a favorable opinion of TRUP’s new CFO appointment, but I am aware that it will be a year before the company’s profitability improves to the mid-teens percentage level.

Company Description

TRUP calls itself a “direct-to-consumer, monthly subscription business that provides medical plans for cats and dogs” on the company’s investor relations website. With respect to market leadership, Trupanion refers to itself as “the largest provider of medical insurance for pets in North America” in its investor presentation slides.

Trupanion derived 66% and 34% of the company’s fiscal 2022 top line from its Subscription (or Direct-to-Consumer/DTC) Business And Other Business (Business-to-Business/B2B segments, respectively as revealed in its 10-K filing. Separately, the US accounted for 84% of TRUP’s FY 2022 revenue, while Canada and other international markets contributed the remaining 16% of the company’s sales for the prior year.

New CFO’s Participation In His First TRUP Earnings Call Is A Key Corporate Development

In the earlier part of this month, Trupanion’s new Chief Financial Officer or CFO, Mr. Fawwad Qureshi, took part in the company’s Q3 2023 results briefing. This is a much more significant development for TRUP than what it seems on the surface.

TRUP’s stock price has more than halved year-to-date in 2023, in contrast with +15.5% rise for the S&P 500 in this year thus far. It is worth paying attention to the fact that Trupanion’s shares actually plunged by -26.7% on March 23, 2023. On the same day, Seeking Alpha News reported that former CFO “Drew Wolff will be stepping down from his position effective June 1, 2023.” It was also disclosed on March 23 this year that the company’s two Executive Vice Presidents for Legal & Regulatory and Pricing, respectively will also part ways with Trupanion. Earlier in January, TRUP revealed in an announcement that “Darryl Rawlings, Founder & Chief Executive Officer, will assume the additional role of Chair of the Board” to “support a smooth CEO succession in 2025.”

As such, Fawwad Qureshi’s appointment as the company’s new CFO in September 2023 and his subsequent participation in the company’s third quarter results call could help to boost investor confidence as TRUP starts to exhibit signs of management stability once again. Notably, Fawwad Qureshi has relevant experience at other consumer-focused businesses, having served as CFO for Nike (NKE) Global Technology and CFO of brands at Expedia (EXPE).

It is also enlightening to look at Trupanion’s competitive edge from the perspective of someone who is new to the company. At its Q3 earnings briefing, the new CFO Fawwad Qureshi shared that TRUP lost less than 10% of 209,000 clients who faced a price hike in excess of +20%.

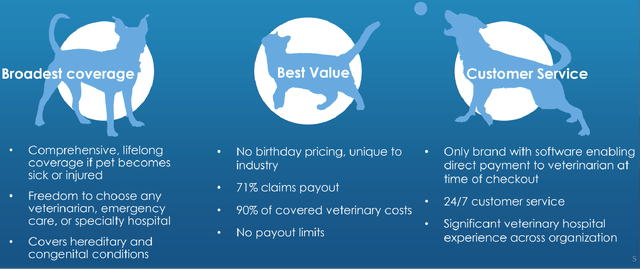

Trupanion’s Value Proposition

TRUP’s Investor Presentation Slides

It is realistic to assume that Trupanion’s value proposition resonates with the vast majority of its customers, as TRUP has been able to keep most of its clients despite imposing a +20% price increase.

Fawwad Qureshi had emphasized at the company’s Q3 2023 results call that the “trade off” involving price hikes and client loss “was certainly financially accretive to top line and more impactful to AOI (Adjusted Operating Income.” In other words, Trupanion’s new CFO has an understanding of how the company could leverage on its bargaining power with customers to make tough decisions (e.g. price increase).

In summary, the new CFO coming on board represents a new beginning for Trupanion in terms of restoring investors’ confidence as it relates to management stability. Moreover, Fawwad Qureshi has worked at other notable consumer businesses, and he seems to have a good appreciation of TRUP’s strengths and how they might be utilized.

Inflation Is A Major Headwind For Trupanion

Trupanion has been implementing price increases as mentioned in the prior section, but it will take more time for price hikes to offset the inflation in medical costs due to a time lag in price adjustment. TRUP’s normalized operating profit margins for its Subscription Business were as high as 13.9% in FY 2020 and 14.3% for FY 2021, but this segment’s adjusted operating margin had already declined to the high single digit percentage level this year based on management disclosures at the most recent quarterly earnings briefing.

At its Q3 2023 earnings call, the company explained that “veterinary inflation increased an additional 900 basis points over historical norms” last year, and noted that it requires “12 months to 18 months to reprice our existing members.” The weak operating profitability for Trupanion is another key reason for the stock’s poor year-to-date share price performance, apart from the issue of management departures as detailed in the previous section of the article.

The market is unlikely to be willing to re-rate Trupanion’s shares in a significant manner until the profitability for its Subscription Business reverts back to 2020-2021 levels. Taking into account TRUP’s guidance of achieving a 15% operating income margin for the Subscription Business segment in a year’s time by Q4 2024, the probability of a meaningful rebound in Trupanion’s shares in the near term is reasonably low.

Closing Thoughts

I am hopeful that the new CFO appointment for TRUP will help to ease investors’ worries about past management departures. On the flip side, I am disappointed with Trupanion’s management guidance that the Subscription Business’ operating margin will only approach or exceed its earlier 2020-2021 levels in the final quarter of next year.

Read the full article here