Welcome to another installment of our CEF Market Weekly Review, where we discuss closed-end fund (“CEF”) market activity from both the bottom-up – highlighting individual fund news and events – as well as the top-down – providing an overview of the broader market. We also try to provide some historical context as well as the relevant themes that look to be driving markets or that investors ought to be mindful of.

This update covers the period through the first week of November. Be sure to check out our other weekly updates covering the business development company (“BDC”) as well as the preferreds/baby bond markets for perspectives across the broader income space.

Market Action

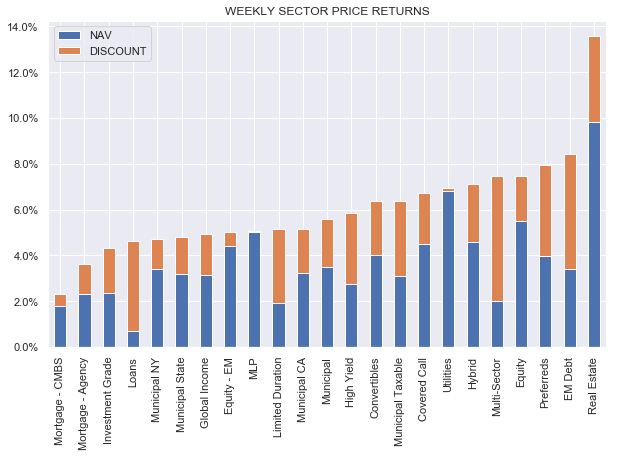

CEFs enjoyed a sharp rebound with all sectors rallying across both NAVs and discounts. REITs were in the lead with a nearly 14% gain. The end-of-Fed-hikes theme managed to drive a relief rally across the broader income market.

Systematic Income

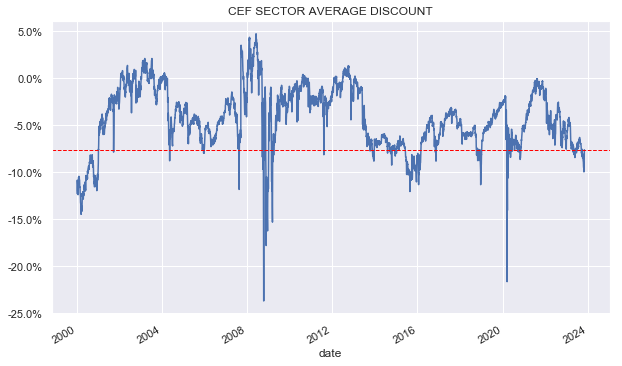

The average discount tightened sharply by around 3%, bouncing off an unusually wide double-digit level.

Systematic Income

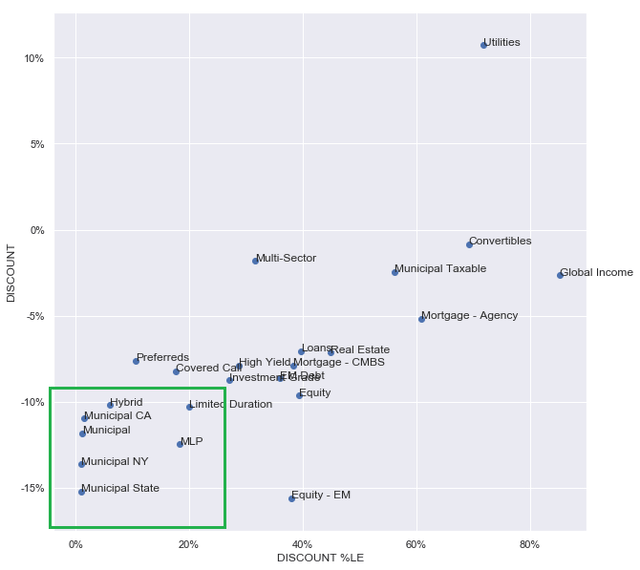

Muni CEF sectors remain historically cheap in discount terms.

Systematic Income

Market Themes

Several First Trust Energy / MLP CEFs (FEN, FEI, FPL, FIF) have announced a merger and, more importantly, a merger into a new ETF EIPI. CEF consolidation has been a theme over the last couple of years with many mergers across CEFs into other CEFs. The reasons are a reduction in fixed costs and improved secondary market liquidity. However, merging CEFs into an ETF is not very common. The main reason is two-fold.

One, ETF fees tend to be below CEF fees, even for active ETFs. And two, ETFs tend to be unleveraged whereas CEFs tend to be leveraged. Since management fees are applied to all assets, an unleveraged vehicle with the same NAV as a leveraged vehicle accrues less fees for the manager because of both of these factors.

The four CEFs have all seen decent discount tightening already however there is still around 7% left to go as open-end funds trade at a discount of close to zero.

There is some chance the mergers may not be approved by the shareholders. It would certainly be odd if that happened given investors would forgo the additional discount tightening but loss aversion is real (investors don’t like losing funds they know) and CEF investors have been known to vote against their interests.

Fund mergers do tend to be successful so these seem like decent tactical opportunities. Given the high volatility of MLP CEFs a safer trade would be to rotate from another MLP CEF into these 4 rather than open up a new position since MLP CEFs could easily give up 7% of NAV due to macro factors.

Market Commentary

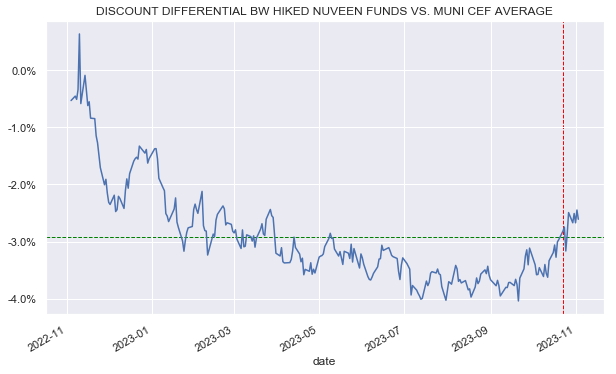

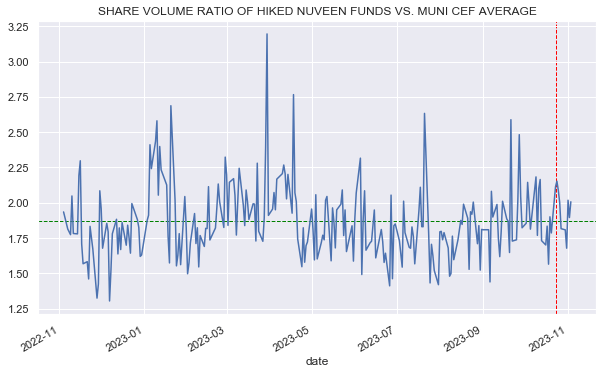

On the distribution front we saw significant hikes for Nuveen Muni CEFs. These hikes are unusual as they were not in response to improved net income but rather intended to drive discount tightening and “support secondary market trading”.

The discount point is quite clear as distribution increases do tend to drive improved valuations. In response to the hikes (marked by a red line) we do indeed see an improvement in Nuveen discounts (for the funds that hikes) relative to the broader Muni CEF sector by close to 0.5% in relative discounts. However, the Nuveen funds in question continue to trade at wider discounts than the sector in absolute terms.

Systematic Income

The secondary market trading point is less obvious as it’s not clear what it means and, if it means an increase in traded volume, it’s not clear that a rise in distribution will necessarily improve this.

Initially we saw a drop in Nuveen fund volumes after the hikes but this was followed by a rebound to a level that is slightly ahead of the previous average volume ratio versus the broader Muni CEF sector.

Systematic Income

Elsewhere, Invesco cut its Muni CEF VPV and hiked the bond CEF VBF. VBF is a curious case since normally a rise in yields would not increase the net income of an unleveraged bond CEF like VBF. It also does not have a lot of short-dated bonds to allow it to organically recycle capital into higher coupon bonds.

What likely happened is that the fund proactively turned over its portfolio from lower to higher-coupon bonds. This doesn’t necessarily increase its portfolio yield but it can drive net income higher.

Finally, Eaton Vance made another trim across limited duration CEFs EVV and EVG.

Stance And Takeaways

CEFs have enjoyed a sharp rally over the last week or so on the back of an expectation of the end of Fed’s hikes. If the Fed has indeed reached the end of its hiking cycle, we could see a further rally across the CEF space. However, until the Fed cuts the policy rate considerably, we are unlikely to see a sustained tightening in discounts given many CEFs, particularly in fixed-income sectors, continue to carry high leverage costs.

Read the full article here