Note:

I have covered Performant Financial Corporation (NASDAQ:PFMT) previously, so investors should view this as an update to my earlier articles on the company.

Back in 2021, I applauded Performant Financial Corporation’s (“Performant Financial”) decision to abandon its legacy student loan recovery business and focus on the rapidly growing healthcare segment:

Company Presentation

While the performance of the new core business hasn’t always lived up to expectations in recent quarters, the company appears to be on the right track as evidenced by last week’s better-than-expected third quarter results with both the top- and bottom line exceeding consensus expectations.

Regulatory Filings

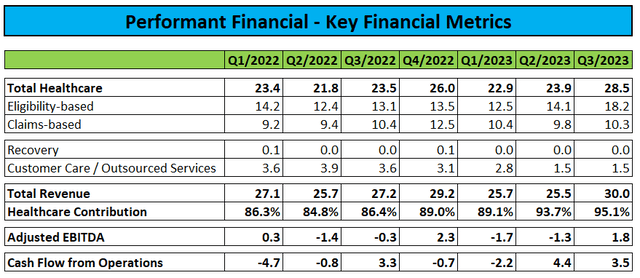

Total revenues of $30 million approached a new two-year high with core healthcare contributions reaching 95% for the first time.

Performant Financial reported Adjusted EBITDA of $1.8 million and generated $3.5 million in cash flow from operations.

Our healthcare revenue enjoyed strong double-digit growth in the quarter led by commercial client growth,” stated Simeon Kohl, CEO of Performant. “Continuing our first half trend, we implemented 12 additional commercial programs in Q3. This brings our 2023 total to 34 implementations. We anticipate these 34 programs will deliver $16 million in annualized revenues at steady state

On the government side of the business, we were excited to announce the New York State Medicaid RAC win in early October. We continue to feel confident in our growth strategy as we have implemented commercial programs at a more disciplined pace and solidified our government footprint with multiple headline wins over the past few years.”

However, results benefited from a pull-forward of eligibility-based revenue as outlined by management on the conference call. Consequently, the company only affirmed previously-communicated full-year projections (emphasis added by author):

We feel confident reiterating our guidance for 2023 health care revenues to the range of $105 million to $110 million, full company revenue between $111.75 million to $118 million and for the full year 2023 adjusted EBITDA to be in the range of $2 million to $5 million which reflects our ongoing investment and growth initiatives, alongside improved operational efficiencies.

Based on current visibility, management expects to achieve “the lower to midpoint of the range” which would be roughly in line with current analyst expectations.

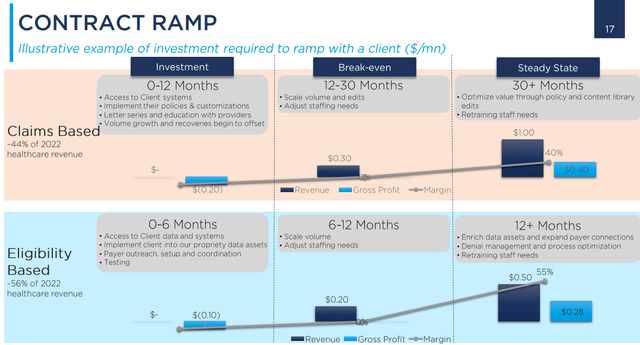

Please note that new contract implementations require an up to 12-month investment phase before reaching break-even levels and even more time to generate substantial profits:

Company Presentation

Subsequent to quarter-end, Performant Financial terminated its existing credit agreement with MUFG Union Bank (MUFG) and entered into a new $25 million revolving credit facility with Wells Fargo Bank (WFC) as outlined in the company’s quarterly report on form 10-Q:

On October 27, 2023 (…), the Company entered into a new credit agreement with Wells Fargo Bank, National Association (…).

The new credit agreement includes a $25 million revolving loan commitment, subject to borrowing base limitations based on a percentage of applicable eligible receivables and contract assets, of which $5.0 million was advanced on the closing date.

A portion of the revolving loan commitment of up to $2.5 million is available for the issuance of letters of credit. (…)

The obligations of the Company under the New Credit Agreement are secured by liens on substantially all of the assets of the Company and each of its existing subsidiaries (…).

The New Credit Agreement matures on October 27, 2026. (…)

The interest rate of SOFR +2.50% to 3.00% represents an improvement from the legacy MUFG credit agreement.

In addition, the new facility is governed by somewhat less restrictive covenants but is subject to a $5 million minimum liquidity requirement.

Performant Financial used a combination of proceeds from the initial advance and cash on hand to repay the $11.25 million outstanding under the MUFG credit agreement.

In addition to providing important covenant relief, the refinancing resulted in an almost $10 million increase in available liquidity. Moreover, the new credit facility contains an accordion feature providing for an additional $10 million in commitments under the facility, subject to certain conditions.

Bottom Line

Following a less-than-stellar first half performance, Performant Financial Corporation reported decent third quarter results with both the top- and bottom line outperforming expectations as well as strong cash generation.

However, the quarter benefited from a pull-forward of eligibility-based healthcare revenues. Based on current visibility, management expects full year revenues and earnings to come in at the lower to midpoint of the range which is in line with consensus estimates.

Perhaps most importantly, the company managed to refinance its existing credit agreement, with a new revolving credit facility providing for greater financial flexibility at substantially improved terms.

With Performant Financial Corporation apparently no longer at risk of missing out on management’s full-year projections and considering materially increased financial flexibility, I am upgrading the company’s shares from “Sell” to “Hold“.

Read the full article here