Introduction

In today’s article, I’d like to discuss the Vector Group (NYSE:VGR), a peculiar company that sells cigarettes, and more recently, develops luxury real estate projects. Yes, you read correctly, this is a company that both sells tobacco and builds real estate! Talk about a mix!

At first glance pairing these two industries under one roof might seem like pairing ice cream with ketchup, it just seems like it can’t make business sense.

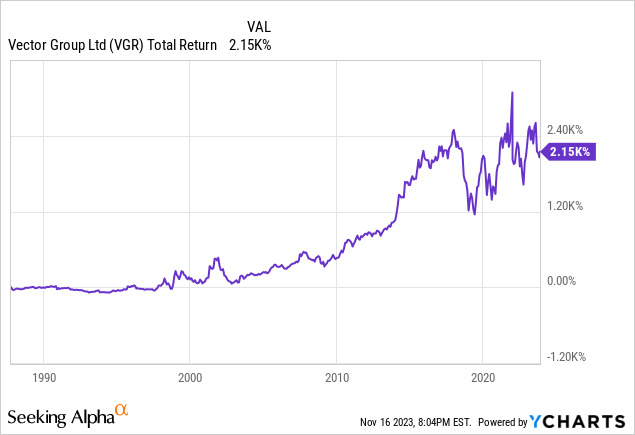

Except it can, I believe the two can go together! I’ll explain the merits of the strategy further on in the article but for now, you can simply look at the total returns generated as some initial evidence that the strategy is feasible.

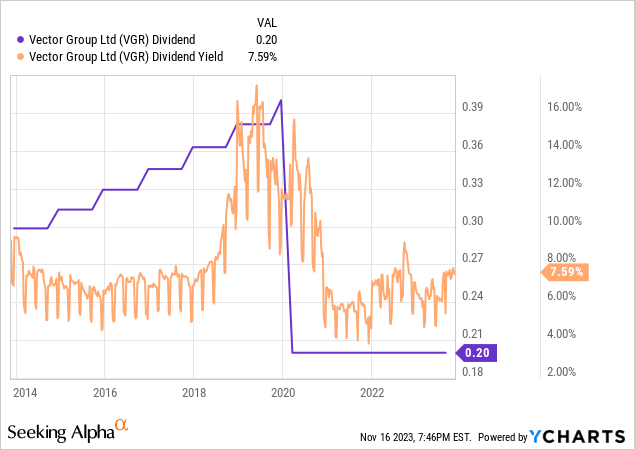

But there are some risks, Vector has historically been a huge dividend payer, it currently offers investors a generous yield of over 7%, a trait common among tobacco stocks including Altria (MO), British American Tobacco (BTI), and Phillip Morris (PM). But of these companies, only Vector Group seems to be aggressively pushing into real estate development.

So while this move is perhaps positive for long-term investors, it does raise the risk of a dividend cut as I will explain later in the article.

If you’re interested in learning more about my views on other tobacco stocks like those I just mentioned I would refer you to the article I wrote comparing Altria and Philip Morris earlier this year.

Company Overview

The Old Tobacco Business

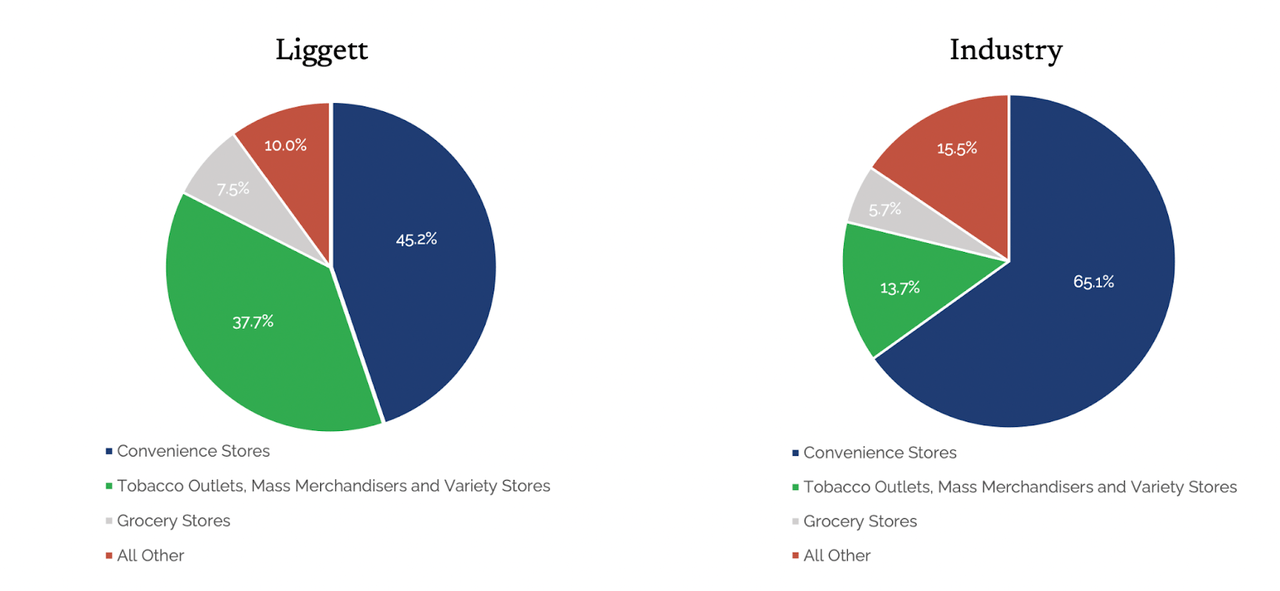

Vector Group’s tobacco strategy is rooted in capturing the value segment of the market, distinguishing itself from higher-end competitors like Marlboro by offering budget-friendly cigarettes.

A key player in executing this strategy is Liggett, Vector’s cigarette business, which significantly increased unit volumes over the past decade, showcasing a commitment to delivering compelling value propositions in the U.S. cigarette industry.

Vector IR

Central to Vector’s strategy is a focus on the discount segment, supported by a differentiated distribution network. Liggett’s deliberate choice to sell cigarettes through tobacco outlets and mass merchandisers, rather than convenience stores, aligns with this strategy, enabling the company to provide more competitive prices to end users.

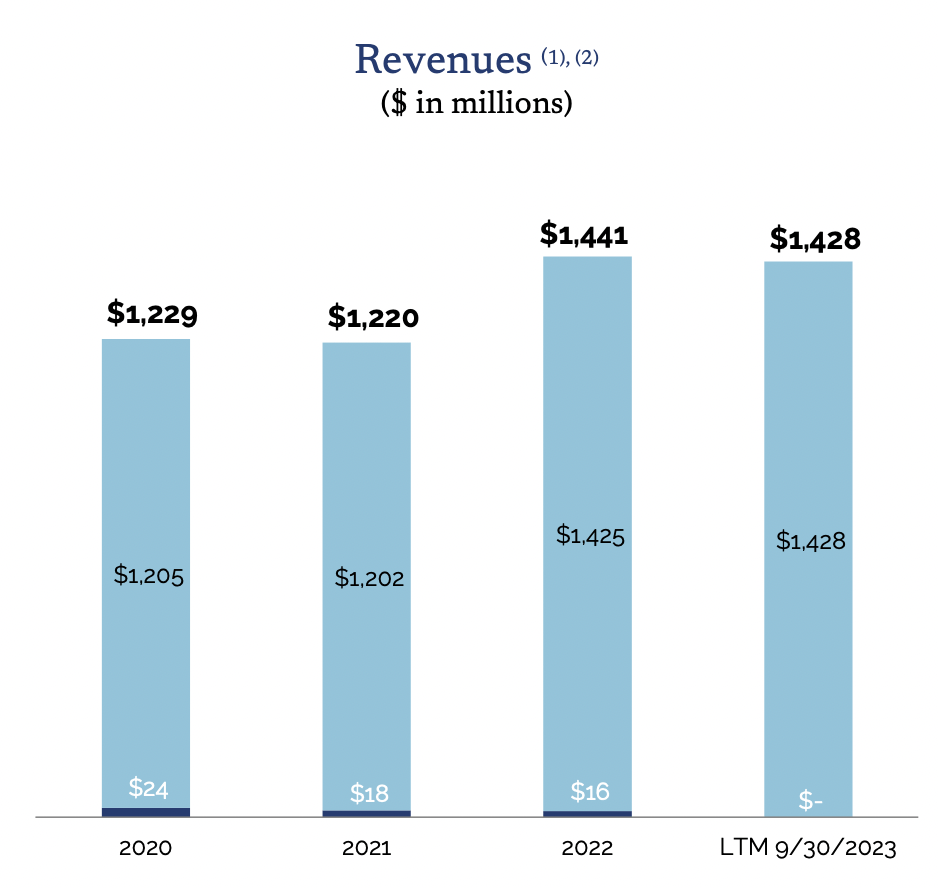

This strategic positioning has translated into solid financial performance, with Vector Group’s tobacco segment reporting an EBITDA of $365.5 million for the twelve months ending September 30, 2023. This financial success underscores the effectiveness of Vector’s strategy, as the company not only captures market share in the value segment but does so with a keen eye on profitability.

In essence, Vector’s strategy of targeting the value segment, emphasizing affordability, and leveraging a tailored distribution network has proven successful, as evidenced by robust financial performance reflected in the substantial EBITDA generated over the last 12 months. This positions the company as a resilient and strategic contender in the U.S. cigarette industry.

The New Real Estate Business

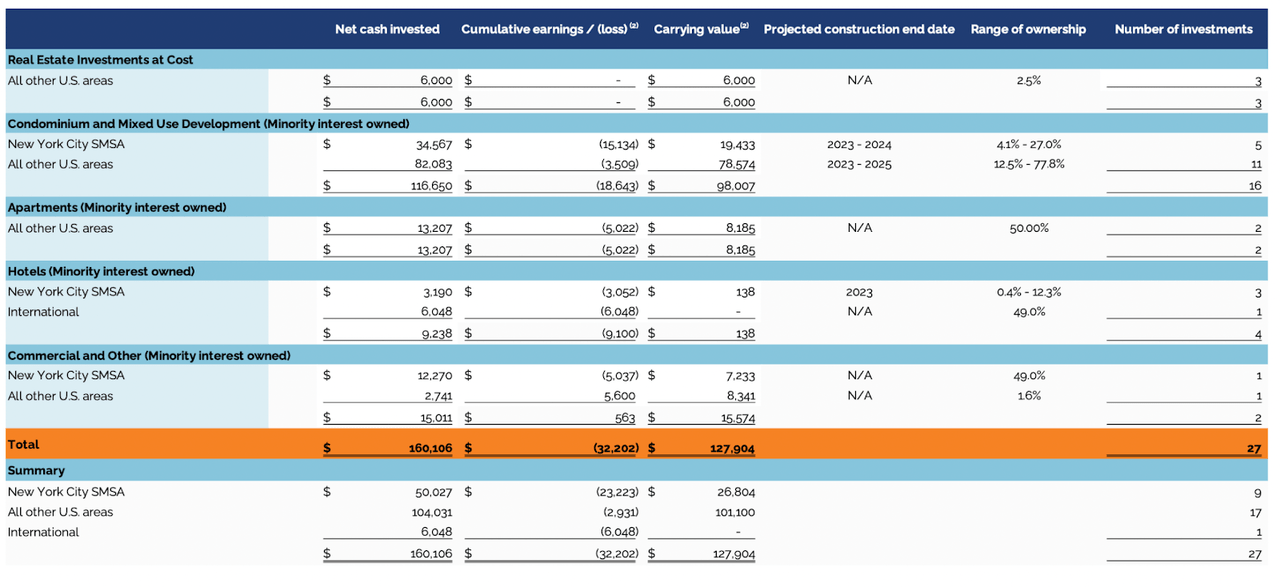

Vector Group’s real estate endeavors, managed through its wholly owned subsidiary, New Valley LLC, reflect a new strategic focus for long-term growth. Diversifying its interests, New Valley holds stakes in a spectrum of real estate ventures, spanning condominium and mixed-use developments, apartment buildings, hotels, and commercial properties. As of September 30, 2023, New Valley has invested approximately $176 million in its real estate portfolio, demonstrating a significant and ongoing commitment.

In 2022, New Valley made significant investments in real estate ventures in fast-growing markets: Raleigh, North Carolina, and Miami, Florida, while also reinforcing existing commitments. The company’s annual report underscores its dedication to deploying capital opportunistically through New Valley to enhance stockholder returns.

Vector IR

In the real estate investment breakdown above, as of the latest data shared, New Valley has a real estate carrying value of $128 million, with a noteworthy 76% ($98 million) invested in condominium projects, particularly emphasizing the New York City market.

It’s essential to recognize that Vector’s real estate business presents a unique risk-reward profile compared to the tobacco industry. While the tobacco business is known for its steadiness, the real estate segment, with its diverse ventures and strategic investments, carries higher risk but also holds the potential for higher rewards.

Vector IR

While relatively small now, Vector’s real estate strategy through New Valley LLC reflects a deliberate and opportunistic approach, aiming for sustained long-term growth while acknowledging the inherent dynamics and potential rewards in the real estate industry. This strategic diversification adds an interesting dimension to Vector’s overall business portfolio.

Tobacco + Real Estate = ???

Using a steady business like tobacco as a funding source for riskier investments, such as real estate, offers distinct advantages. The stable cash flow from the tobacco industry acts as a reliable financial backbone, helping to mitigate the risks associated with the volatility of real estate, and providing a cushion for potential losses.

Moreover, the reliable revenue stream allows for patient and strategic planning in real estate investments, focusing on sustainable growth. It provides diversification without overreliance on any single venture, fostering a balanced and resilient business portfolio.

This, perhaps strange, approach combines stable income with growth potential.

The historical resilience of the tobacco industry during economic downturns adds further value. The demand for tobacco products tends to remain steady, providing a financial cushion during challenging economic times. This resilience enables the company to weather economic uncertainties while maintaining the ability to invest strategically in real estate throughout all market cycles.

Risk to Dividend Investors

Vector’s increased focus on real estate investments, while potentially promising for long-term growth, introduces a measure of risk for investors seeking high dividends. Real estate, being inherently riskier, may demand capital unexpectedly, impacting the predictability of dividend payouts.

Unlike the stable cash flow from the tobacco industry, the real estate market’s volatility and the need for additional capital during unforeseen circumstances can increase uncertainty. The shift to real estate poses risks for dividend-centric investors, but it’s important to note that this strategy could potentially be a more efficient use of cash, fostering capital appreciation and overall portfolio growth in the long run IF the company proves it can execute.

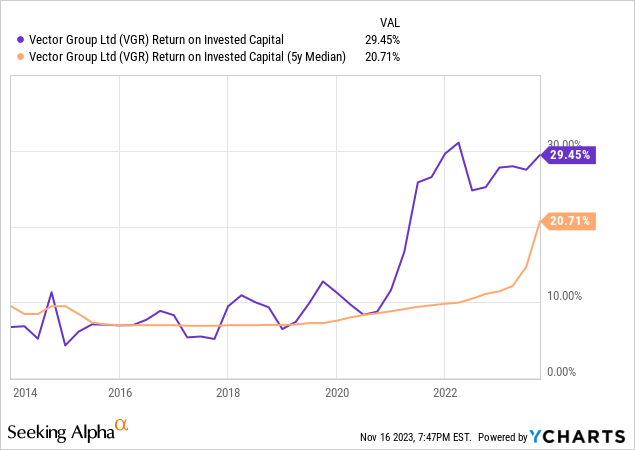

Returns on Invested Capital

As you can see above the company maintaining more cash flow for reinvestment into the business may not be such a bad thing after all as the company boasts phenomenal returns on capital (upwards of 20%!). The massive shift upward happened after COVID-19 and may be a result of high inflation pushing smokers to purchase cheaper brands of cigarettes to pinch pennies.

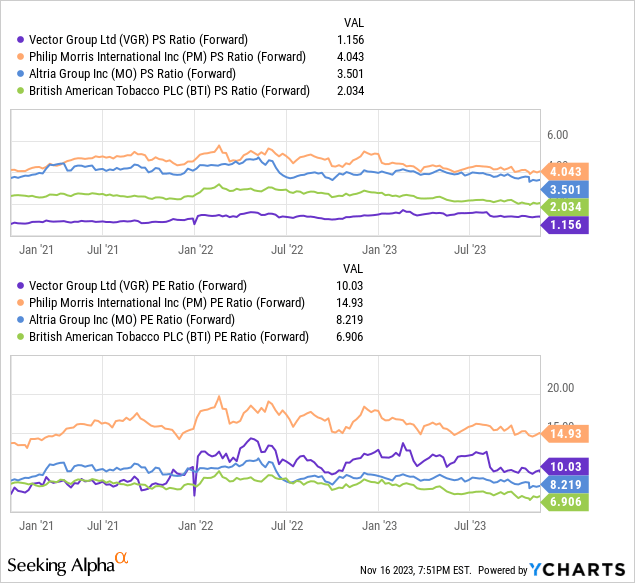

Valuation

On the valuation front, looking at the price to forward sales estimates, Vector Group is the cheapest by far, trading at just 1.15X sales, Philip Morris and Altria trade for roughly 3X as much at 4x and 3.5X sales respectively. Things look a bit less rosy comparing future earnings against peers as Vector Group trades around 10x earnings whereas British American and Altria trade at Just 6.9X and 8.2X respectively. Only Philip Morris, at 14.9X, is priced more richly.

But let’s not get carried away a 10X multiple on earnings is still dirt cheap, this equates to a 10% earnings yield, that much higher than what you can get from bonds. Additionally, I believe its lower PE ratio and higher PS ratio simply indicate that the company has more room to scale than its larger peers, something it has had a proven track record of doing. Finally, the real estate play is unique in the industry and may be a unique avenue for Alpha.

Conclusion

Vector is a tobacco business like no other, its real estate endeavors offer a totally unique avenue for growth which seems to be overlooked by the market.

With Liggett, they’ve mastered the art of capturing the value segment in tobacco, boasting resilient financial performance. Yet, the company’s foray into real estate, led by New Valley, introduces a wild card. While tobacco offers a steady beat, the unpredictable nature of real estate poses a unique risk.

For those with greater risk appetite, such as myself, I believe Vector could make a great deal of sense to include in one’s portfolio. The combination of stability, value, and growth is very attractive to me.

As such, I rate Vector Group a “Strong Buy”.

Read the full article here