Investment Thesis

IonQ’s (NYSE:IONQ) Q3 2023 results reinforce the following narrative that IonQ is a fast-growing business, but that its stock is far from cheap. This is only for investors with a very long-term horizon.

I characterize this investment approach as follows: It appears to be a high-risk, high-reward venture initially. However, the typical scenario involves investors assuming significant risks from the start. The stock inevitably experiences a downturn, leading investors to hold on in hopes of recovering their initial investment, only to eventually let go.

I’m not promoting an everlasting buy-and-hold strategy either. While that may suit investors with perfect hindsight, I advise caution against investing more in IonQ than one is comfortable holding through both the downturns and upswings.

To summarize my stance succinctly, I argue that this investment at this valuation is only for investors with a real ability to buy and forget mentality and to do so with only a small amount of their portfolio, as a venture-like investment strategy.

Quick Recap,

In my previous analysis, I said,

[…] this is a story stock and not a viable business, at least not yet. Yes, there are very strong revenue growth rates. And yes, there’s more than enough capital on its balance sheet to support its vision. But nevertheless, this is a story stock and investors should keep this in mind when investing.

I have a buy rating on this stock, as I believe that IonQ has strong potential. But at the same time, I make ample references to the fact that this stock is beyond expensive. Therefore, proceed with caution.

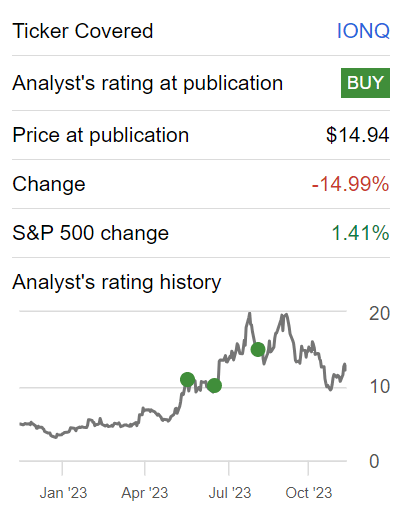

Since I made that statement, the stock has been a poor performer, as you can see below.

Author’s work on IONQ

And yet, I don’t believe this detracts from my contention that it is a very richly valued story stock. And that investors seeking exposure to IonQ are paying a premium for a compelling narrative and that they should expect to remain bullish on this name for a very long number of years, patiently, to get rewarded on this stock.

IonQ’s Near-Term Prospects

IonQ is a company dedicated to the advancement and commercialization of quantum computing hardware and software. The company employs trapped-ion technology, a method that utilizes individual ions as quantum bits (qubits) to execute quantum computations.

Moving on, IonQ’s sales pipeline has significantly expanded throughout the year, and since the start of 2021, IonQ has anticipated exceeding its goal of reaching cumulative bookings of $100 million by the end of 2023. Recently, IonQ sold four quantum systems, surpassing its earlier projection of possibly selling a full quantum system by the end of 2023.

IonQ’s commercial and technical momentum continues to accelerate exceeding initial expectations. During the earnings call, the AQ 64 system, in particular, is highlighted as a key component of IonQ’s path to commercial advantage.

Furthermore, IonQ has diversified its offerings with the introduction of AQ 64 Tempo systems and AQ 35 Forte Enterprise Systems, catering to different customer needs and applications. Notably, IonQ has made substantial strides in quantum networking, as exemplified by a significant $25.5 million deal with the United States Air Force Research Lab.

On a bearish aspect, IonQ business model is inherently lumpy. Achieving sustained growth and maintaining momentum in the rapidly evolving field of quantum computing poses ongoing challenges, as you not only need the company’s technology to be ready, but customer demand to be high. The transition from academic origins to a product-driven company requires meticulous engineering efforts.

Additionally, IonQ faces the complexities associated with quantum networking and error mitigation. These considerations, when taken together with the departure of IonQ’s Co-Founder in Chief Sciences Chris Monroe, are likely to bring additional bumpiness to its growth rates, a key matter we discuss next.

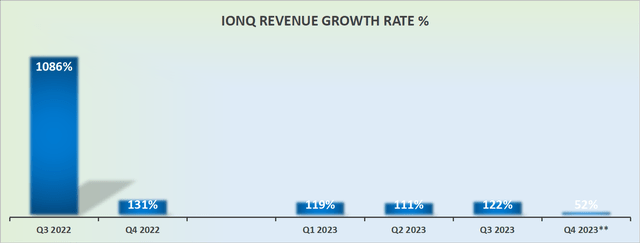

Revenue Growth Rates Expected to Decelerate

IONQ revenue growth rates

IonQ’s growth rates are expected to decelerate. Even if IonQ beats revenue estimates by over 20% as they did in the recently reported Q3 results, the fact remains that its revenue growth rates are expected to decelerate.

What’s more, one cannot make the case that it’s the law of large numbers, since we are still referring to a business that’s on a run-rate of meaningfully less than $50 million of revenues.

The problem with investing in IonQ is that this investment is highly subjective. For this investment to work out reasonably over the next year or so, one needs a particularly bullish backdrop. That being said, over a longer-term horizon of 3 to 5 years, I believe that IonQ could be well set up for a rewarding investment as it appears to be making all the right moves.

The problem, at its core, is one of valuation.

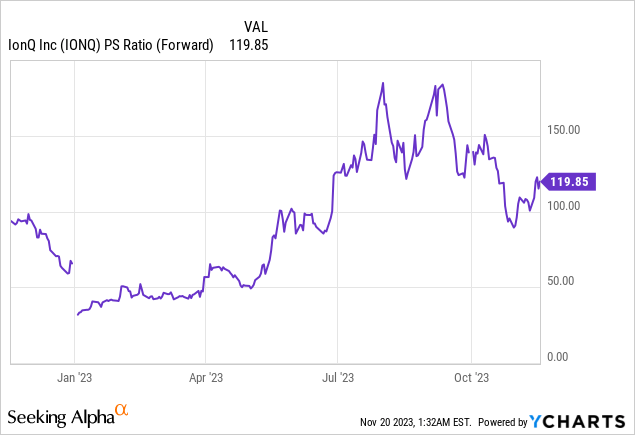

IONQ Stock Valuation — Expensive

IonQ’s stock is priced at more than 110x forward sales. Also, IonQ is burning through approximately $20 million of free cash flow per quarter. Given that its revenues are still less than $10 million per quarter, this means that for every $1 of revenues, IonQ is burning through $2 of cash.

I understand that IonQ is investing for strong and stable future growth, but for now, this is not a viable business model.

Management makes the case that while they are filing with the SEC, they have no intention of diluting shareholders. Indeed, even if IonQ is on path to burn more than $80 to $100 million of free cash flow over the next 12 months, IonQ holds about $460 million of cash and equivalents on its balance sheet.

This means that aside from a potential acquisition along the way, IonQ has a very strong cash position that will provide it with a solid foundation for the business to continue investing for growth for a good number of years.

The Bottom Line

IonQ presents itself as a high-risk, high-reward investment that demands a patient, long-term horizon from its shareholders.

The stock’s current valuation is steep, and its performance has reflected this premium. However, for investors with a genuine ability to adopt a buy-and-forget mentality and a willingness to endure the inevitable downturns and upswings, IonQ could prove to be a rewarding venture over an extended period.

IonQ’s business model, while showing strong revenue growth rates, is challenged by inherent lumpiness, potential disruptions from key personnel departures, and the expectation of decelerating growth rates.

On the positive side, IonQ is well-funded, boasting a robust balance sheet with over $450 million in cash and equivalents, providing a solid foundation for continued investment in growth. Despite its current expensive valuation and cash burn rate, IonQ’s strategic moves in the quantum computing space may position it favorably over the long term, making it a compelling option for investors with a patient and risk-tolerant investment strategy.

Read the full article here