Lockheed Martin (NYSE:LMT) is one of the largest and most well-respected defense contractors on earth.

Responsible for a huge number of Land, Air, Sea, and Cyber combat systems in western arsenals today, the company plays an incredibly important role in the security and defense posture of much of the western-leaning world, including the United States and its allies.

In the air, Lockheed manufactures the F-22 Raptor fighter jet, the F-35 Lightning stealth jet, and countless other helicopter, missile, and support aircraft systems that are currently in use across several branches of armed forces across the globe.

At sea, Lockheed produces numerous warships and naval combat systems for the U.S. and other allied navies.

On land, Lockheed manufactures the widely publicized HIMARS system which has performed well in Ukraine, in addition to a number of other rocket and radar systems that support allied troops in a number of different combat environments.

Finally, in the cyber realm, Lockheed produces a number of integrated SIGINT, electronic warfare, and simulation products that support critical defense infrastructure and combat systems across the globe.

Lockheed’s defense contracting prowess has translated to strong financial results.

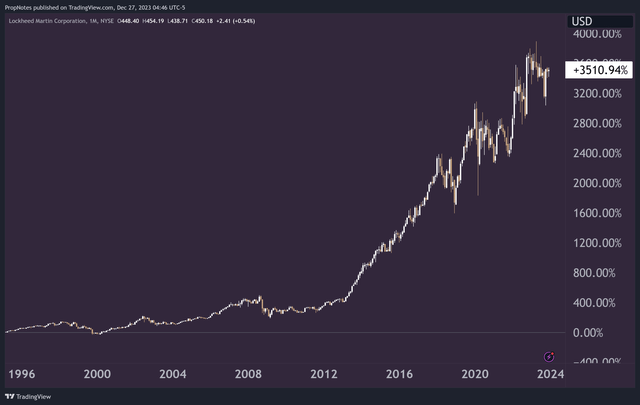

Since going public in 1995, LMT investors have enjoyed more than 3,500% in total returns as revenue and net income have skyrocketed:

TradingView

Yet, despite this incredible run, we still think shares look attractive.

Today, we’ll discuss the top 3 reasons why you should own LMT, and why the company remains a compounder-class stock after all these years.

1.) Stable & Improving Financials

The first major drawing point of LMT is the company’s stellar financials.

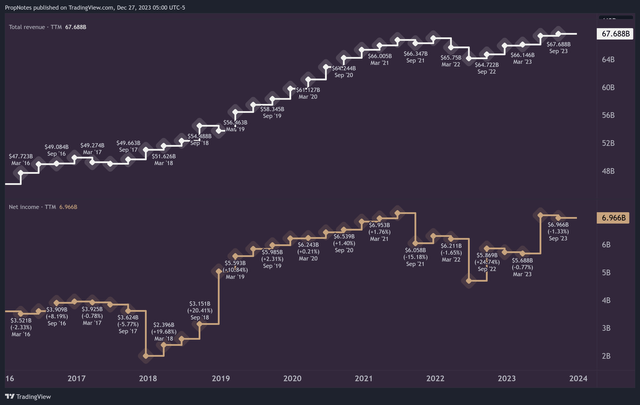

Since 2016, TTM sales have grown from ~$47 billion to >$67 billion in almost a straight line, which represents a compounded annual growth rate of more than 5%:

TradingView

While this may seem low, on such a large base, and for a company dealing in industrial (hardware) defense products, it’s actually quite impressive.

TTM Net income has been bumpier but has also seen considerable gains over the same span, growing from $3.5 billion at the beginning of 2016 to ~$7 billion today. This represents an even more impressive CAGR of 10.4%, which shows LMT’s ability to accomplish better cash conversion and achieve economies of scale.

Driving these results is an incredibly strong product moat.

Presently, defense manufacturing in the U.S., which is LMT’s largest customer, is decided on a contract-bidding system. Some have decried this system as a forum for abuse, fraud, and cost gouging on the part of defense contractors, and this certainly has happened in the past.

However, on the whole, consolidation among defense contractors is a logical conclusion to the winner-take-all contract awarding mechanism, and thus effectively competing for contracts becomes more and more competitive over time, as orders become larger and more complex.

Right now, LMT’s largest advantage is that it is a trusted defense contractor.

The size, scope, and scale of the contracts it has been awarded are massive, and in turn, the ability of LMT to win future contracts improves for every contract it wins.

With a long contract pipeline and best-in-class engineering talent, LMT has a strong product moat it can leverage to bolster top line results into the future.

Finally, from a liquidity standpoint, LMT’s balance sheet is in great shape. The company has more than 23 billion in current assets. Plus, with only 17 billion in long term debt, the company’s ability to pay its bills and maintain operations is very strong.

Top to bottom, LMT continues to produce strong financial results on the back of its product moat, strong defense relationships, and engineering prowess.

2.) The Valuation

Despite the company’s strength and ability for increasing the scope and profitability of its business over time, shares right now present an interesting opportunity.

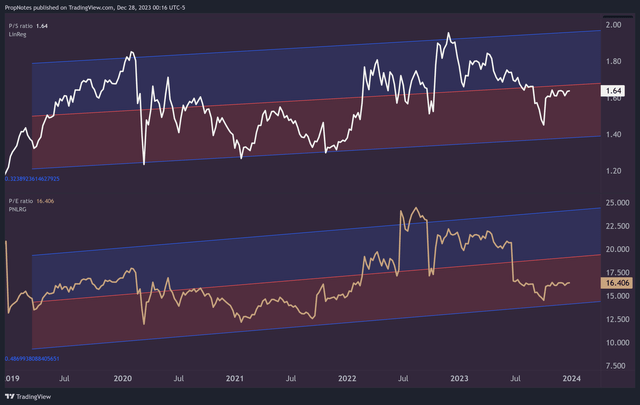

Currently trading below its historical valuation on both a top and bottom-line basis, LMT looks attractively priced:

TradingView

As you can see above, the 1.64x sales multiple and 16.4x earnings multiple are both trading below the long-term linear regression line, which indicates that now, on balance, is a better time than not to buy into a position in LMT.

On a broader basis, at 16x, LMT’s P/E is lower than that of the S&P 500, which currently trades around 24x earnings.

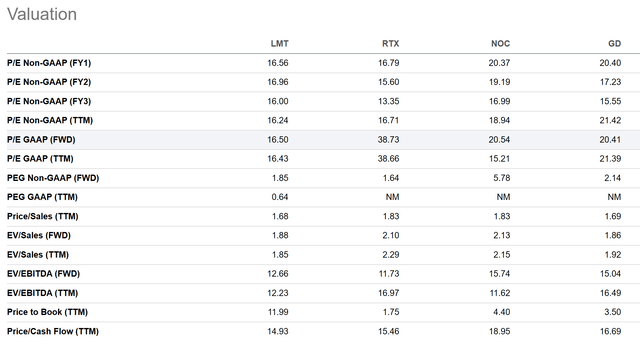

Finally, LMT also trades beneath the multiples of its defense sector peers, including RTX (formerly Raytheon) (RTX), Northrop Grumman (NOC), and General Dynamics (GD):

Seeking Alpha

Sporting a lower FWD P/E ratio, cash flow multiple, and sales multiple, LMT is definitively the cheapest company in the defense peer group at the present moment.

All in all, on a historical, broad, and peer valuation basis, LMT looks attractively priced.

3.) Capital Returns

Sure, the financials are strong, and the valuation looks attractive. But how does an investment in LMT actually make money?

This is where we come to point #3: LMT is returning capital to shareholders at a breakneck pace.

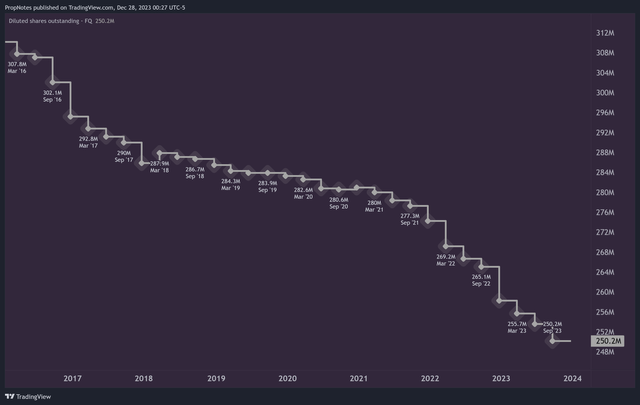

First, the company is buying back shares at a solid clip:

TradingView

Since 2016, LMT has reduced the number of diluted shares outstanding from more than 300 million to less than 250 million, a decrease of nearly 20%.

Remember, when a company retires shares, it means that your ownership in the business increases without you having to do anything.

In other articles, we have often argued that the best companies to invest in are companies that are increasing top- and bottom-line results, while reducing share count. The combination of an increase in demand for shares, coupled with a declining supply of shares creates a powerful engine for capital appreciation, and consequently, wealth building.

LMT is well positioned from this standpoint.

Additionally, LMT sports a safe, well covered, growing dividend.

Right now, LMT only pays out ~50% of its profits as a dividend, which gives the company significant room to operate, as well as potentially increase this ratio in the future.

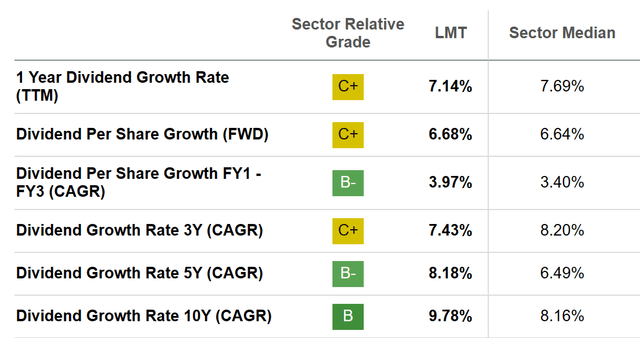

In addition, LMT has been growing its dividend since 2002. While the growth of the payout has been slowing as LMT has saturated the market and become more mature as a company, LMT’s 10-year dividend CAGR still stands at nearly 10%:

Seeking Alpha

These long-term growth rates are above the industry median, which shows that LMT has stronger operational leverage available to return capital to shareholders.

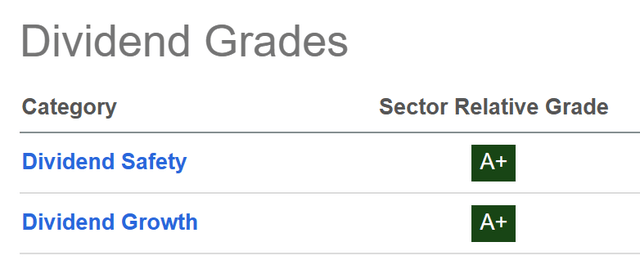

Plus, LMT is one of only 9 companies covered in the Seeking Alpha dividend grade universe that has an A+ for both Dividend Safety and Dividend Growth, while also yielding more than 2%:

Seeking Alpha

Between the buybacks and the dividend growth, LMT has an incredibly strong capital returns profile that, when combined with the strong financials and attractive valuation, turns the stock into one of our favorite stock ideas for the long term.

Risks

That said, there are some risks to this thesis.

Key among them being the direction of U.S. Fiscal Spending.

In their own words, here’s what LMT says about fiscal spending:

With nearly three quarters of our sales from the U.S. government, U.S. government spending levels, particularly defense spending, and timely funding thereof can affect our financial performance over the short and long term.

Right now, the company remains sanguine about U.S. fiscal prospects and the prioritization of defense spending in the national budget.

However, that could change in the future:

usdebtclock.org

With a national debt totaling nearly 34 trillion, we will eventually need to begin making choices, as a country, about what does and doesn’t get priority in terms of spending. This may eventually come to harm defense budgets, which means that LMT’s top and bottom-line growth is, to some degree, constrained by the U.S. government.

That said, this issue seems a long way off, and remains probable, not certain. Thus, it shouldn’t damage an investment thesis at this juncture.

Other risks that are common with equities, including wars, international conflicts, natural disasters, etc, don’t really apply with LMT, as the company is well insulated, and often benefits, from strife and conflict.

That means that it can act as a natural hedge in a portfolio in the event of global issues that may arise.

Thus, while LMT does face some potential risks to growth in the future on the back of U.S. fiscal constraints, it trades that risk for a lower risk set vs. the average U.S. equity.

Summary

All in all, LMT looks like a great investment right now, due to its strong financial performance and product moat, attractive valuation, and solid capital returns policy.

There are some far-off risks, like the U.S. debt, which may curtail growth in Federal defense spending.

However, on the whole, LMT’s risk profile is acceptable, especially given that the company actually benefits somewhat from global issues.

We rate LMT a “Strong Buy”.

Cheers!

Read the full article here