Introduction

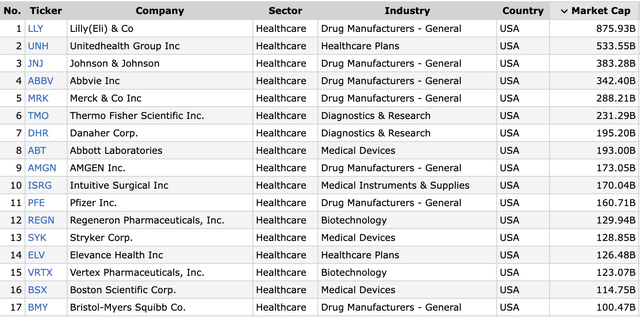

Did you know the U.S. is home to 17 stock-listed healthcare companies with a market cap of at least $100 billion? Four of these companies have a market cap of more than $300 billion, with Eli Lilly (LLY) being the leader with a market cap closing in on $900 billion.

FINVIZ

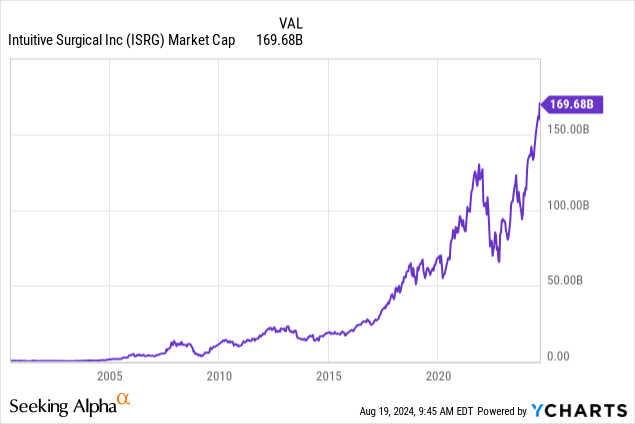

One company on that list (nr. 10) is Intuitive Surgical (NASDAQ:ISRG), a company I called “One Of The Biggest Compounders In Healthcare” in my last article on January 26.

Since that article, ISRG has returned 28%, beating the 14% return of the S&P 500 by a wide margin.

As spectacular as that may be, it’s even more impressive if we consider that ISRG was worth roughly $50 billion before the pandemic hit. Ten years ago, the company had a market cap of less than $25 billion. In other words, ISRG’s market cap has grown 7x in roughly ten years!

In this article, I’ll update my thesis, explain why the ISRG stock seems to know no gravity and tell you what I make of the current risk/reward.

So, let’s get to it!

Innovation-Driven Growth

Intuitive Surgical operates in the medical instruments industry. However, it’s not just one of many players but one that dominates the market of healthcare robots.

These robots allow for “minimally-invasive” care, meaning surgery with limited collateral damage. This is a win-win for healthcare providers and patients, as it increases efficiency.

Intuitive Surgical

Currently, the company has three platforms, Da Vinci SP, Da Vinci Xi, and Ion.

The first Da Vinci system was launched in 1999. I added emphasis to the quote below:

Da Vinci systems offer surgeons three-dimensional, high definition (“3DHD”) vision, a magnified view, and robotic and computer assistance. They use specialized instrumentation, including a miniaturized surgical camera (endoscope) and wristed instruments (e.g., scissors, scalpels, and forceps) that are designed to help with precise dissection and reconstruction deep inside the body. – ISRG 2023 10-K

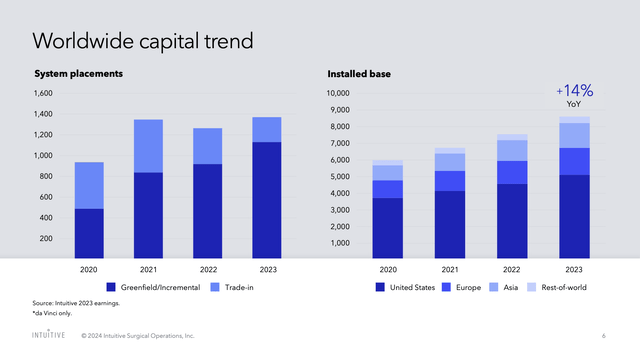

The demand for these products is strong. Since 2020, the installed base has risen by 14% per year.

Intuitive Surgical

So far, it does not look like this trend is stopping.

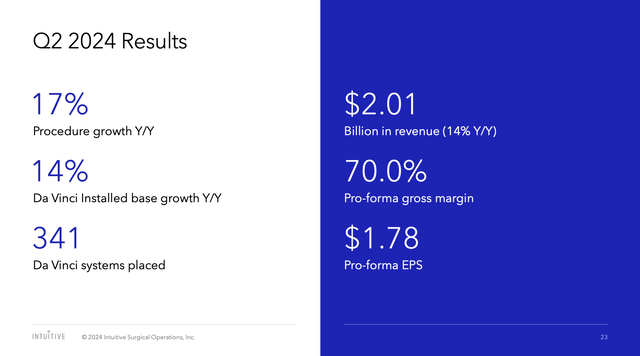

For example, in the recently released second quarter, the company’s revenue surged by 14%, driven by a 17% increase in procedures.

According to the company, the global procedure growth was led by key surgical procedures like cholecystectomy, colon resection, lung resection, and foregut procedures.

Thanks to strong demand, the company placed 341 Da Vinci systems in the quarter, including 70 units of the new Da Vinci 5 system. During its call, the company noted that the rollout of da Vinci 5 is progressing well, with customer feedback praising its improvements in precision, imaging, ergonomics, and integration, all of which resulted in improved operational efficiency.

Intuitive Surgical

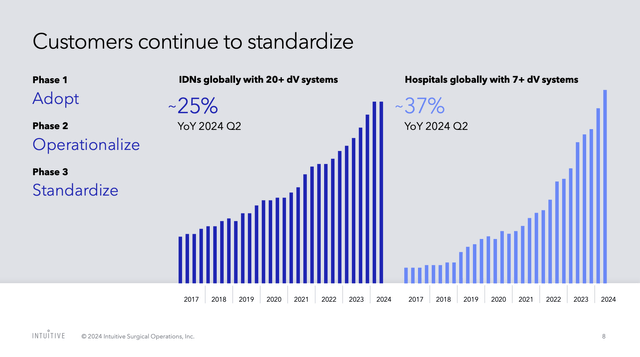

The company’s products are so popular that the number of buyers with multiple systems is growing exponentially as well.

For example, the number of hospitals with more than seven Da Vinci systems has grown by 37% in the second quarter. The last time the company saw a quarter-on-quarter decline in these numbers was back in 2020.

Intuitive Surgical

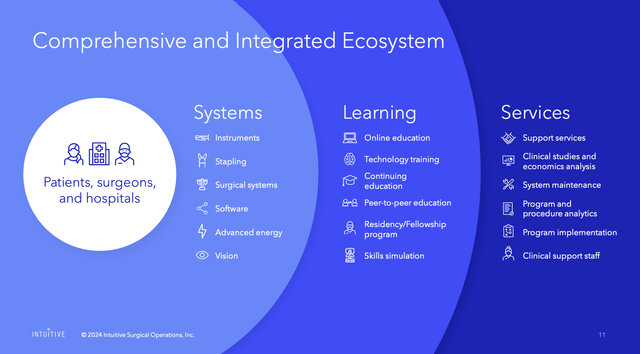

It also helps that ISRG benefits from much more than just the sale of a “piece of equipment.”

The company is building an entire ecosystem, which includes significant long-term sales after the delivery of a system. As we can see below, this includes:

- Education, trading, and similar learning services.

- Support services.

- Clinical studies/economic analysts.

- System maintenance.

- Clinical support staff.

Intuitive Surgical

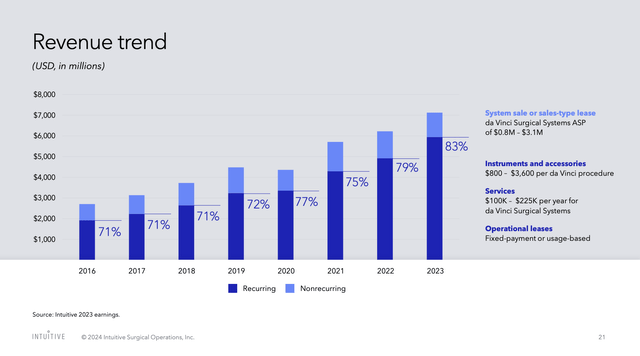

In addition to providing value-added services, this provides the company with another major benefit: recurring revenue.

If there’s one thing investors are looking for, it’s companies with recurring revenues. For example, selling someone a car is a one-time sale. Selling someone a subscription to a streaming service is recurring revenue.

For companies, a higher recurring revenue share increases revenue visibility and lowers overall volatility.

In 2016, Intuitive Surgical had 71% recurring revenue. This included accessories, services, and operational leases. Last year, recurring revenue accounted for 83% of its total revenue.

Intuitive Surgical

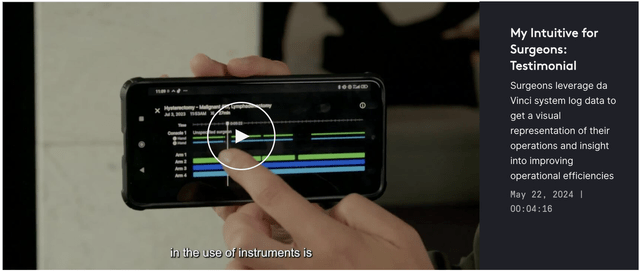

One major part of providing better services is its digital ecosystem. According to the company, the adoption of the My Intuitive app, which expanded to almost 14,000 surgeons, and the doubling of Intuitive Hub usage year-over-year are a great example of the growing importance of digital tools in surgery.

Essentially, digital solutions like Case Insights provide analytics that help to improve surgeries. This includes reducing time to proficiency and improving overall clinical outcomes.

On top of improving healthcare, it also builds a stronger connection between ISRG and its customers. Once you’re in their ecosystem, it is much harder to leave. It’s like owning five Apple products. Once you’re in their system, it’s hard to leave.

Intuitive Surgical

Needless to say, the company is confident that by prioritizing product quality, surgeon adoption of key procedures, and operational efficiency, it is not only supporting its market position but also laying the foundation for long-term success.

Where’s The Shareholder Value?

Thanks to strong growth in procedures, the second quarter saw 14% revenue growth to $2.2 billion. Excluding exchange rate changes, revenue growth was 15%.

As I already briefly mentioned, this was supported by 17% more procedures and a 14% bigger Da Vinci installed base.

Intuitive Surgical

Moreover, the launch of Da Vinci 5 has contributed to higher average selling prices of $1.44 million per system in the second quarter, up from $1.39 million in 2Q23.

Adding to that, the Ion platform, which is designed for minimally invasive lung biopsies, saw 82% more procedures, with 72 new systems placed in the second quarter.

It also helps that despite sticky inflation, the company reported a pro forma gross margin of 70%, which is an improvement from 68.5% in the same quarter last year. This was due to cost reductions, lower inventory reserves, and leverage of fixed overhead.

Furthermore, ISRG maintains a fantastic balance sheet. This balance sheet includes $7.7 billion in cash and investments, up from $7.3 billion in the first quarter of this year. The company, which does not pay a dividend, uses its cash position to lower financial risks fund R&D, strategic M&A, and manage share buybacks.

This year, analysts expect the company to end the year with $5.0 billion in net cash, meaning more cash than gross debt. That number is expected to rise to $10.9 billion in 2026. Although this is subject to events like buybacks, M&A, and unexpected investments, it shows how healthy the ISRG balance sheet is.

Speaking of analyst expectations, Wall Street is very upbeat about ISRG’s future.

Based on the FactSet data from the chart below, here are the expected EPS growth rates through 2026:

| Date | EPS Growth |

| 2023 | 22% |

| 2024E | 17% |

| 2025E | 15% |

| 2026E | 17% |

Not bad, right?

Now comes the bad news.

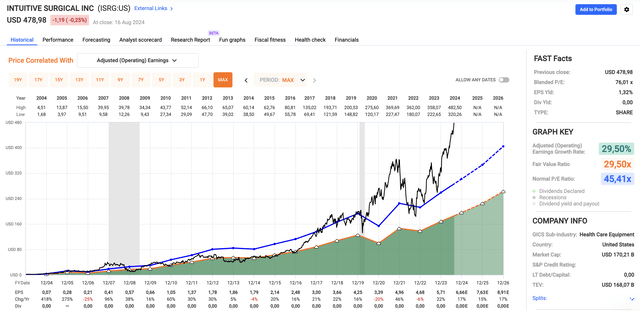

As we can see below, ISRG trades at a blended P/E ratio of 76.0x. This is a mile above its normalized P/E ratio of 45.4x (the blue line).

FAST Graphs

Although I expect ISRG to generate double-digit EPS growth for many years to come, paying 76x earnings is a tough pill to swallow.

The current consensus price target is $482. While I am writing this, ISRG trades at $481.

Regardless of how bullish I am on this space, I would not be a buyer of ISRG at these levels, as too much good news has been priced in.

Takeaway

Intuitive Surgical continues to impress with its innovation-driven growth, strong financials, and market-leading product portfolio.

I believe the company’s dominance in the healthcare robotics space, combined with a growing ecosystem of recurring revenues, positions it for long-term success.

However, the stock’s current valuation, trading at a very lofty P/E ratio, suggests that much of the good news is already priced in – at least in the mid-term.

While I’m bullish on ISRG’s future, I recommend patience. At these elevated levels, it may be smart to wait for a more attractive entry point before considering an investment.

However, if I were long, I wouldn’t change anything, as I don’t like to sell winners.

Read the full article here