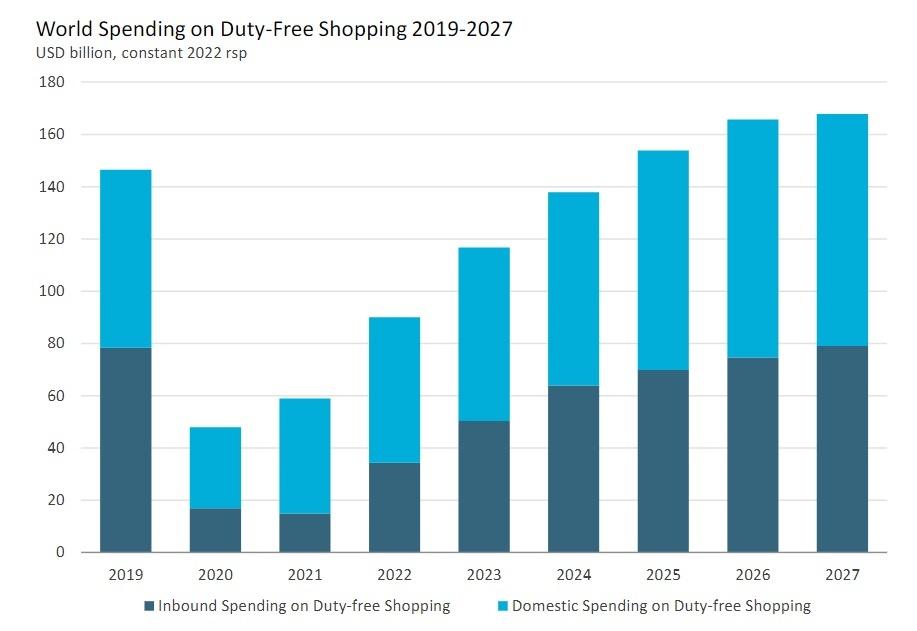

After a major collapse during the Covid pandemic, the duty-free market is back on a growth spurt and is expected to recover to 2019 levels by 2025—and forecast to reach $168 billion by 2027, according to new data by market research provider Euromonitor International.

However, by 2027, duty-free sales (international and domestic combined) will only be 15% above its pre-crisis levels. This amounts to incremental growth of $51 billion from 2023 to 2027, and the recovery of international duty-free will lag behind domestic.

The growth is being fueled by surging air traffic bringing shoppers back into airport and downtown stores worldwide. A new feature of the post-pandemic environment is how domestic spending on duty-free shopping has become the dominant force in the channel (see chart below)—with locations like China’s duty-free island of Hainan taking a large slice of the market during the pandemic, and hanging onto it.

Prudence Lai, senior analyst at Euromonitor International, commented: “Duty-free is intrinsically linked to tourism flows. The pandemic resulted in a plunge of almost 70% in 2020 in the world duty-free market as travel halted. However, travel is now back, with Asia Pacific markets, especially China, reopening borders in 2023.”

China’s reopening is the most significant. International duty-free spending by the Its country’s nationals represented $11 billion in 2019 according to the research data, contributing to 20% of global outbound duty-free spending. By 2027, China is expected to account for one quarter of all international duty-free sales, amounting to $18 billion at constant 2022 prices.

China remains a dominant force

If the Euromonitor forecasts prove correct—given other crucial impacts like the current cost-of-living crisis and crippling inflation don’t skew the data—then the Chinese will wield even more power in the retail channel they dominated before the pandemic.

As well as extending their reach in the international duty-free channel to a whopping 25%, they will also have a powerful influence in expanding the downtown duty-free business in China itself, and helping to revive markets like South Korea, Japan, and Thailand, three destinations that have traditionally been top-of-mind for Chinese travelers looking to shop.

Across these Asian locations, the biggest influence on the balance shift has been domestic duty-free sales in China. Lai said: “Hainan is the hottest hub for luxury brands to penetrate the China market after Covid-19. Brands establish their presence through unique omnichannel, immersive and personalized in-store experiences to appeal to sophisticated Chinese consumers.

“For example, La Mer opened its largest boutique in April 2023, enabling a first-of-its-kind omnichannel experience including in-store spa services. Hainan is far from being a mature market as brands keep investing in this strategically important Chinese domestic shopping haven.”

Asia Pacific’s domestic duty-free sales are forecast to reach $81 billion by 2027, dominated by China, which will account for 87% of the regional total. China has now embarked on the creation of duty-free designated destinations like Hainan province in other parts of the country.

The Hainan experiment, started many years before the pandemic, but came into its own during the health crisis because China’s zero-Covid policy brought international travel to a standstill. This left many Chinese with no option but to shop for duty-free goods domestically in places like Hainan rather than Paris, London and New York.

Extending the domestic duty-free concept while China’s borders reopen gives Chinese nationals the convenient option of shopping at home or going abroad to buy luxury, but not necessarily achieving the savings they might once have done versus shopping duty-free in their own market.

Read the full article here