By James Smith

Investors think the UK has a bigger inflation challenge than the US or eurozone

When we asked our clients in a recent webinar, 73% of roughly 200 respondents thought the UK had a bigger inflation problem than the US or eurozone. They aren’t alone.

Markets see rates peaking above 6% later this year, and far from pushing back against those lofty expectations, the Bank of England doubled down with a surprise 50 basis-point rate hike last month. And if that message hadn’t sunk in enough, Governor Andrew Bailey went further by suggesting markets were prematurely pricing rate cuts – a particularly hawkish statement, when you consider that markets expect Bank Rate to be at or above current levels for the next two years.

Above all, the latest decision and subsequent comments reflect a growing loss of confidence and patience in the Bank’s models, but also the forward-looking inflation indicators that have been pointing in a better direction for several months now. It’s pretty clear that the next few decisions will be guided by actual inflation and wage growth data, and probably not a lot else.

The decision also suggests that the Bank isn’t done yet. Previously the bank’s more gradualist and pragmatic approach to rate hikes suggested we were very close to the peak. But having returned to 50bp rate hike increments, it’s highly unlikely the committee will be content with holding rates at current levels, or only hiking once more by 25bp, in August.

Admittedly, we aren’t convinced the 50bp move will be repeated, but we think two further 25bp moves in August and September are likely – and we wouldn’t rule out more. Remember that one of the Bank’s two arch-doves also left the committee last month, and early signs suggest her replacement will be more hawkish.

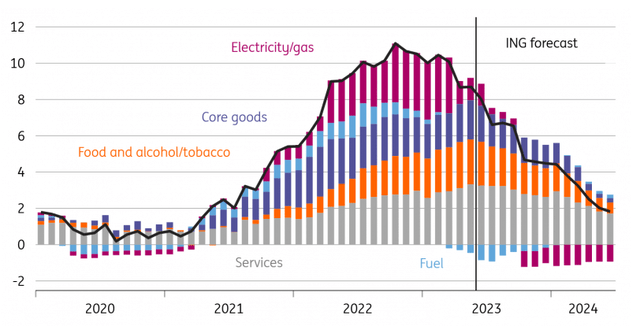

Sticky UK services inflation means headline CPI has been higher than expected

Macrobond, ING calculations

Inflation data should look a bit better by the autumn

Whether or not the Bank ends up delivering the five extra rate hikes priced into markets heavily depends on whether the inflation numbers show some improvement over the summer. At the headline level they should, though mainly because a 20% cut in household energy bills this month will shave off roughly one percentage point from annual CPI.

In theory, this matters little, but policymakers have put a lot of store in inflation expectations surveys over the past year or so, and the fall in electricity, gas and petrol prices has helped drive these down among consumers and businesses alike. Indeed the plunge in natural gas prices should start to show through in lower services inflation, albeit gradually. By November’s meeting, we think there will be sufficient evidence for the Bank to finally end its hiking cycle. Ultimately most – though not all – of the UK’s inflation drivers are shared with other developed market economies.

Either way, Bank Rate close to 6% is very restrictive by historical standards. Higher loan-to-income multiples mean that mortgage repayments are now equivalent to roughly 35% of average disposable income. That’s a bigger share than when rates peaked ahead of the global financial crisis.

Admittedly most mortgages are fixed for at least two years, which means most households are yet to encounter higher repayments. That means a recession isn’t inevitable, but we will see an ever-increasing drag on the UK consumer. The bigger risk in the short-term arguably comes from corporates (particularly small firms), which are typically on floating interest rates and are feeling the squeeze most acutely right now.

Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here