The stock market, as measured by the S&P 500 Index

SPX,

began the new year with a sharp correction, but now it has climbed back to near all-time highs. A new 52-week intraday high was just registered this morning. If the the S&P 500 can clearly break out over 4,800 (a two-day close, for example), the bulls would clearly regain the upper hand. The all-time highs of January 2022 are a closing high at 4,796 and an intraday high at 4,818. Those are well within range at the moment.

There is support just below 4,700, at last week’s lows. Below that is more significant support at 4,600. But if the S&P 500 should fall below 4,550 (the December lows), that would be a very negative development. There is an old adage that if the market falls below the previous December’s lows during the first quarter of the following year, it’s a bear market at that point.

There has been some internal deterioration in the market as a whole, but the most bullish items at the moment are the S&P 500 chart itself and the volatility complex, which has not blinked during the recent market correction. Let’s go over the indicators individually.

First, there is a McMillan Volatility Band (MVB) sell signal in effect. That has a target of the lower -4σ “modified Bollinger Band,” which is currently at 4,615 and rising. It would be stopped out if the S&P 500 were to once again close above its +4σ Band, which is well into all-time high territory, at 4875 and rising.

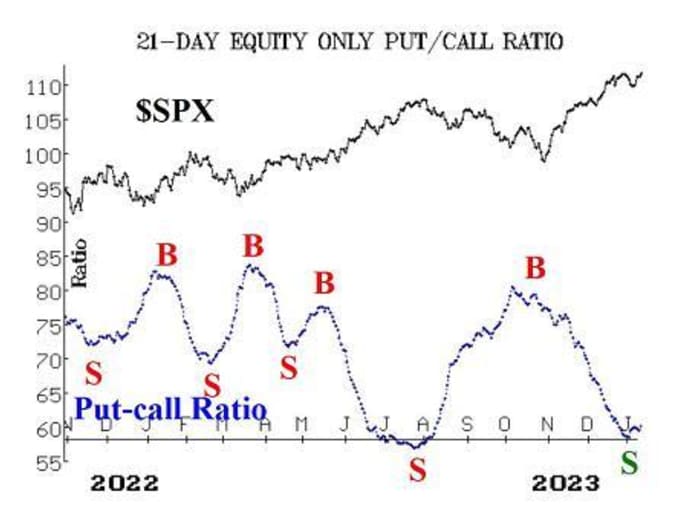

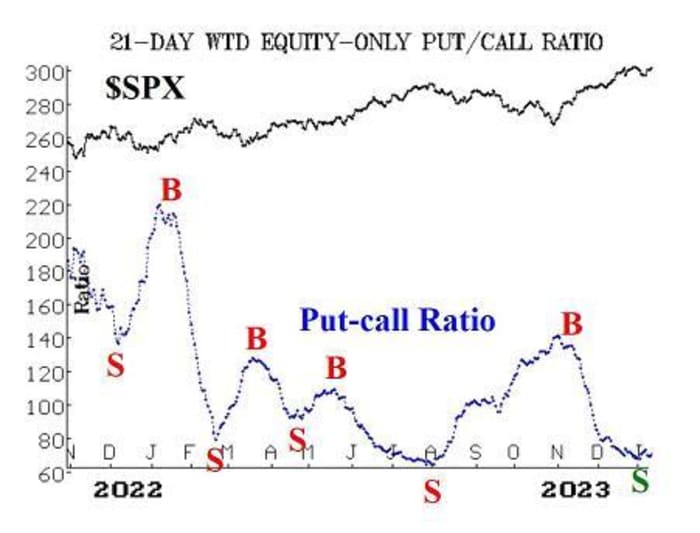

Equity-only put-call ratios are on sell signals, since they have begun to rise after bottoming out near their yearly lows last week. When these ratios are rising, that is bearish for stocks. If the ratios should drop back to new relative lows, then these sell signals would be canceled out. In both cases (standard and weighted put-call ratios), our computer analysis programs agree with the sell signal, despite the “wiggle” on the charts over the past couple of days.

Market breadth has been struggling. It is one of the internal indicators that has not kept pace with the strength of the S&P 500. As a result, both of our breadth oscillators are on sell signals at the current time, and those signals have been confirmed over multiple days. Admittedly, these oscillators are those most “flighty” of our indicators and are often subject to whipsaws. Regardless, they are negative at this time.

A more positive picture is presented by the NYSE New Highs vs. New Lows. New Lows are increasing in number at a slow rate, but New Highs continue to outnumber New Lows on a daily basis. Thus, this indicator remains positive. The bullish signal here would be stopped out if New Lows exceed New Highs on the NYSE for two consecutive days.

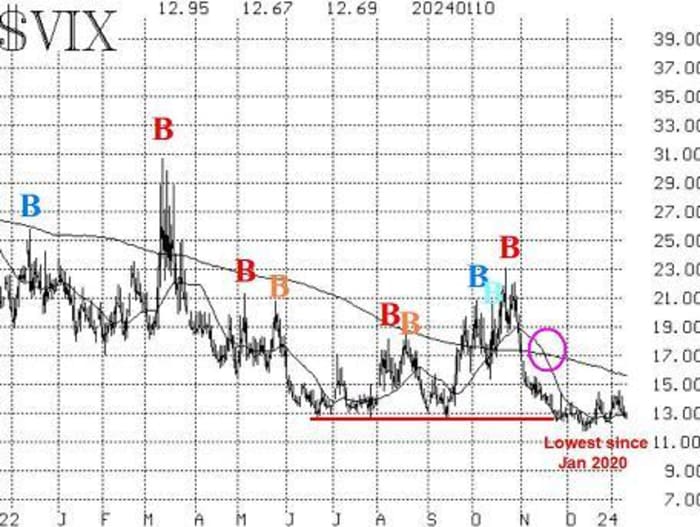

This brings us to the world of implied volatility, which has been bullish throughout the last few months. VIX

VIX

VX00,

has remained low, even when the S&P 500 corrected last week. The trend of a VIX buy signal remains intact. That would be stopped out if VIX were to close above its 200-day moving average, which is currently at 15.60. So, unless that happens, there is nothing for the stock market to worry about.

Included in the implied volatility complex is the fact that the construct of volatility derivatives continues to display a bullish attitude toward stocks as well. The warning sign in this area would come if January VIX futures (the front month) were to close at a higher price than February VIX futures. That has not even remotely been the case, as February continues to trade approximately one point over January.

Realized volatility has not been as bullish, though. The 20-day historical volatility of the S&P 500 (HV20) rose above 10% last week, and that is a sell signal for stocks. That sell signal would be stopped out if HV20 were to fall back and close below 9%. It has not retreated though, even with the S&P 500 rallying, so the sell signal is still in place.

There is a bearish seasonal period coming up, beginning today and lasting for 10 trading days. That is followed by a strong bullish seasonal period. We will be trading both. See the Market Insight for further information on this seasonal trade.

In summary, we continue to hold a “core” bullish position, because of the position nature of the S&P 500 chart, which remains in an uptrend. We are trading other confirmed signals around that “core,” as they occur.

Market insight: The ‘January Defect‘

This particular system is centered around the fact that there is usually a market correction in the middle of January (after the initial new deposits have been invested by institutions), and it is most evident in tech stocks. Hence, the trading system is to short the Nasdaq-100 Index

QQQ

at the close of the eighth trading day of January and to cover the short at the close of the 18th trading day of January.

We have been tracking this seasonal trade for 29 years. There have been both spectacular gains and losses from this system, but since we trade it with options, we can control our risk. In 2022, the system showed a strong profit when the Nasdaq-100 fell 1,900 points over that time frame, as the bear market of that year was beginning. Last year was the opposite: There was nowhere to hide when the Nasdaq-100 was strong throughout the month of January.

In theory, the system enters its position by buying QQQ puts at the close of the eighth trading day of January, which is today, Jan. 11. In reality, the best entry point has varied over the years, so we are going to enter in stages. Overall, the best performance results percentagewise, have come from entering on the 12th trading day. The median gain (for the short sale) from entering on the 12th trading day has been 0.8%.

However, the largest gains (and some of the larger losses, too) have come from entering on the eighth or tenth trading days. The average gain for entering on those days has been nearly 4%; although the average loss has been 3.3% from those entries.

At the close of trading on Jan. 11 and Jan. 18 (the 8th and 12th trading days of January, respectively), Buy 1 QQQ Feb (2nd) at-the-money put.

Your total position will thus be two long QQQ puts, which might each have a different striking price. With regard to taking partial profits, sell the first put that becomes 20 points in-the-money, and roll the other down when and if it becomes 20 points in-the-money. Sell all the remaining puts at the close of trading on the 18th trading day of January — Friday, Jan. 26.

Note, at the close of the 18th day, the other January seasonal trade will begin, but we will discuss that in a later issue of this publication.

New recommendation: SPY straddle buy

In early November, the S&P 500 was toying with resistance on its way up — at the 4,400 level. We bought a straddle, figuring that if the index were to break through to new highs it would accelerate to the upside. However, if there were a failure at that resistance level, the ensuing correction could be swift. Moreover, SPY

SPY

options were not expensive since the VIX was near 13. As it turned out, it was the upside move that occurred, and we jettisoned the puts as the upside break took hold. We still own calls that have been rolled up from that original straddle purchase.

It seems that we are facing a similar situation right now. The S&P 500 is toying with resistance at all-time highs near 4,800. A clear breakout to the upside is sure to cause some short covering and a rapid ascent is likely. However, if the market fails at this level again, sellers will surely be in force, because it might seem that a long-term double top is in place. The VIX is still low, near 13. So, we are going to recommend a straddle buy once again.

Buy 1 Feb (16th) at-the-money call and Buy 1 Feb (16th) at-the-money put: We are going to use a “money” stop here. The straddle costs about 14, so if it has lost 50% of its original value at any day’s close, stop out. Meanwhile, roll either option if it becomes eight points in-the-money.

Follow-up action:

All stops are mental closing stops unless otherwise noted.

We are using a “standard” rolling procedure for our SPY spreads: in any vertical bull or bear spread, if the underlying hits the short strike, then roll the entire spread. That would be roll up in the case of a call bull spread or roll down in the case of a bear put spread. Stay in the same expiration and keep the distance between the strikes the same unless otherwise instructed.

Long 0 ES Jan (19th) 60 calls: were stopped out when ES

ES,

closed below 61 on January 9th.

Long 4 XLP

XLP

Jan (19th) 72 calls: Raise the stop to 71.20.

Long 1 SPY Jan (19th) 477 call: This position was initially a long straddle. It was rolled up, and the puts were sold. The calls were rolled up twice more. This is, in essence, our “core” bullish position. Roll the calls up every time they become at least eight points in-the-money.

Long 2 TECH Jan (19th) 70 calls: We will hold as long as weighted put-call ratio is on a buy signal. The buy signal is still in place, but it’s extremely overbought, so set a stop to sell these calls if TECH

TECH,

closes below 71.

Long 1 SPY Feb (16th) 477 call and short 1 SPY Feb (16th) 497 call: This spread is based on the “New Highs vs. New Lows” buy signal. We will stop ourselves out of this position if New Lows on the NYSE exceed New Highs for two consecutive trading days. Otherwise, there is no price stop based on SPX. The spread has been rolled up previously.

Long 4 UNM Mar (15th) 45 calls: We will hold this position as long as the weighted put-call ratio of UNM

UNM,

remains on a buy signal.

Long 1 SPY Feb (16th) 480 call: This call was bought in line with the Cumulative Volume Breadth (CVB) buy signal. The entire premium is at risk here, since there really isn’t a stop-out for this trade. Sell these calls if SPY trades at 482 at any time.

Long 10 ESPR

ESPR,

Feb (16th) 3 calls: The stock reported the resolution of some pending litigation, and the market had hoped for a better settlement, so the stock sold off. The closing stop remains at 2.25.

Long 2 DIS June (21st) 90 puts: we will hold these puts as long as the weighted put-call ratio of DIS

DIS,

is on a sell signal.

Long 1 SPY Feb (16th) 469 put and Short 1 SPY Feb 16th) 449 put: Was bought in line with the McMillan Volatility Band sell signal. It will reach its target if SPX trades at the -4σ Band, and it will be stopped out of SPX closes above the +4σ Band.

Long 1 SPY Feb (16th) 469 put and Short 1 SPY Feb 16th) 449 put: Was bought in line with the HV20 sell signal. It will be stopped out if the 20-day historical volatility of SPX (HV20) falls below 9%.

Long 1 SPY Feb (16th) 469 put and Short 1 SPY Feb 16th) 449 put: Was bought because the Santa Claus Rally failed this year. We are going to modify the stop slightly: stop yourself out SPX closes above 4800 for two consecutive days.

All stops are mental closing stops unless otherwise noted.

Send questions to: [email protected].

Lawrence G. McMillan is president of McMillan Analysis, a registered investment and commodity trading advisor. McMillan may hold positions in securities recommended in this report, both personally and in client accounts. He is an experienced trader and money manager and is the author of the best-selling book, Options as a Strategic Investment. www.optionstrategist.com

©McMillan Analysis Corporation is registered with the SEC as an investment advisor and with the CFTC as a commodity trading advisor. The information in this newsletter has been carefully compiled from sources believed to be reliable, but accuracy and completeness are not guaranteed. The officers or directors of McMillan Analysis Corporation, or accounts managed by such persons may have positions in the securities recommended in the advisory.

Read the full article here