When I first began following Birchcliff Energy (OTCPK:BIREF) (A Canadian company that reports in Canadian currency) this company was a dry natural gas producer just like Peyto (OTCPK:PEYUF) and Advantage (OTCPK:AAVVF). These companies were operating in the same basin as well. Birchcliff has those low operating costs like the other competitors. But Birchcliff management at the time was an aggressive growing company that was not afraid to take on debt. The acquisition of rich gas production from (what is now) Ovintiv (OVV), which used to be Encana, gave this company a jump in the transition to rich gas. It also resolved a high debt ratio situation as basically, the company sold stock to purchase the acreage. It, therefore, has a larger presence than the other two in liquids production. That may give the company a helping hand with profits in the near future.

Gordondale Asset

I covered this acquisition in a previous article some years back. This asset got the company out of a debt jam as the company raised the money for the asset by selling stock to pay for the purchase.

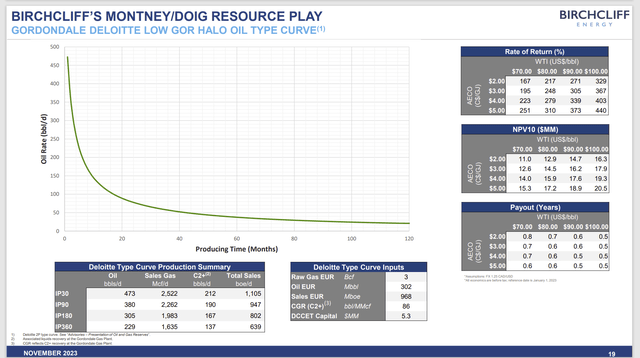

Birchcliff Energy Presentation Of Gordondale Well Profitability (Birchcliff Energy Corporate Presentation November 2023)

The company has made its cost of this acreage back several times over since the purchase. AECO prices went on to crash a few years after this. But the company sailed through with the liquids produced on this acreage.

To this day, the acreage competes successfully with the dry gas production in the area. But more importantly, until sufficient transportation out of the area was established for many of these natural gas producers, the liquids production enabled sufficient cash flow at a time when more than a few producers suffered from lower natural gas prices and issues specifically in Canada.

Now Canada is expecting that some export ability will be available in 2025 with more on the way a few years later. But oil prices are strong and this company produces a significant amount of oil and related products to enjoy a profit advantage in the current environment.

Investors need to remember that with the constant commodity price volatility, any reasonable strategy should work over time. But different strategies predominate at different times. Right now, a rich gas strategy appears to be the superior profit opportunity.

Peyto and Advantage have both begun a gradual transition to more liquids. This company bought its way to rich gas acreage and that acreage came with midstream assets as well. So, the company is a little further along than the other two.

Profitability

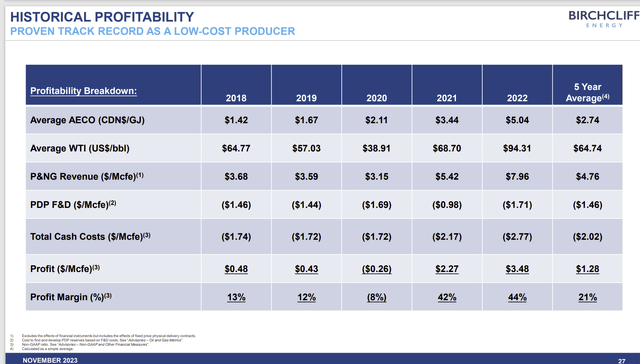

The company’s profitability definitely shows that this company is a low-cost producer.

Birchcliff Energy Profitability History (Birchcliff Energy Corporate Presentation November 2023)

The liquids production should make this company very profitable in the coming years as oil prices are expected to remain decent for some years to come.

The risk, of course, is to not allow costs to get out of line so that losses are run during the downturn. Fiscal year 2020 was extreme. But that year also serves as a warning to keep costs as low as possible.

Generally, the market cares about average profitability throughout the business cycle. Therefore, management cannot “fall in love” with results during the good times because the next downcycle would then be in a position to undo those great results.

Further muddying cost results is that management can leave some products in the natural gas stream and sell the natural gas if the commodity market prices do not justify pulling some products out of natural gas to sell separately.

That means that there is a matrix of prices and a variety of costs available to management to really make comparisons difficult for the average observer.

Growth Story

This company emphasizes growth over income. Although lately, the company has been paying a C$.20 per share quarterly dividend. That is a recent departure from the past.

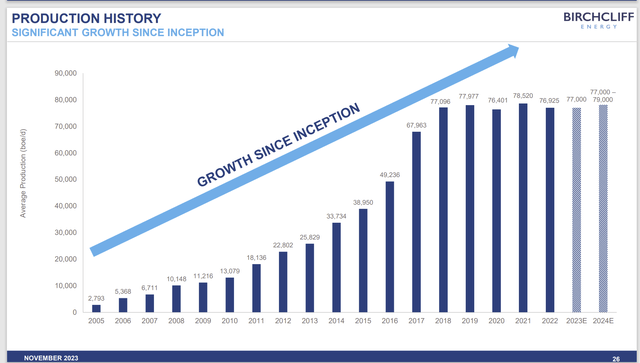

Birchcliff Energy Production Growth History Since Inceptions (Birchcliff Energy Corporate Presentation November 2023) Birchcliff Energy Production Growth History Since Inception (Birchcliff Energy Corporate Presentation August 2023)

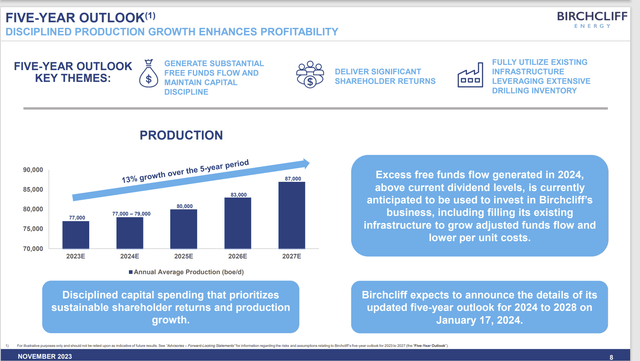

Of course, the last five years have been anything but favorable to growth. Still, the guidance would appear to indicate that growth is about to resume assuming better industry conditions lie ahead in the immediate future. Management has plans underway to construct a new gas processing facility. That should imply that growth will resume.

Management will also take some care with the balance sheet in the future as the debt issues that happened in the past are still a consideration for management.

Management Change

Jeff Tonken, Chief Executive Officer and Chairman Of The Board, will be retiring as CEO. He was the CEO since inception. Therefore, this is big news as this is really the first CEO transition since the company went public.

The new CEO and President is Chris Carlsen. The new CEO inherits a company on the cusp of benefitting from the ability to export natural gas. That should enable the North American market to gradually join the stronger world pricing market. This could well make any natural gas production far more profitable than it has been for a very long time.

Total Company

Management aims to keep a flexible outlook by maintaining a balance between the various parcels owned. This management, like many Canadian companies, owns a significant amount of midstream gathering capabilities and processing plants that link up to long-haul pipelines that get the products to market.

Management did announce that they will accelerate about C$20 million originally part of the 2024 Capital budget into 2023 to take advantage of the heating season prices.

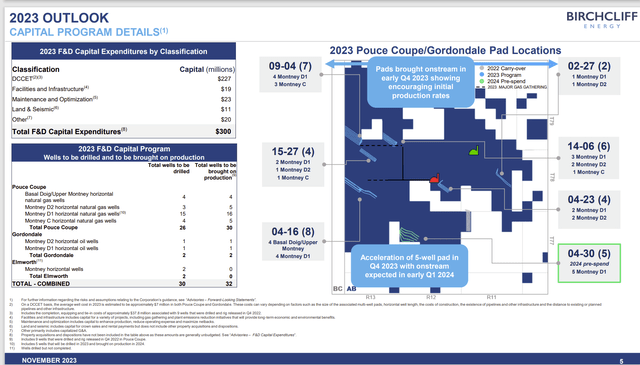

Birchcliff Energy Summary Of Capital Expenditures by Area (Birchcliff Energy Corporate Presentation November 2023)

The different acreages compete for capital under different industry conditions. Usually, the Gordondale assets have the first call due to the profitability of the asset and the liquids production.

The current environment appears to make Gordondale a better deal than anyone could imagine as commodity pricing at the time of the purchase was far lower than it is now. Natural gas prices were also headed lower in the near future as well. But the next few years should prove that purchase to be an incredible bargain that one seldom sees.

Birchcliff Energy Five Year Plan (Birchcliff Energy Corporate Presentation August 2023)

Should prices remain strong (and that is always a huge if), then this company is set to reward shareholders handsomely. Just remember that this is an extremely low-visibility industry with a lot of volatility.

This management is a little more willing to add debt to the balance sheet and run a higher debt ratio than some others I follow. That did, in the past, lead to the purchase of Gordondale (effectively for stock) to resolve the issue the last time around.

With the change in the CEO position, shareholders will have to see what the company’s debt and growth strategy will be going forward.

This company is probably a strong buy for traders who are disciplined enough to get out of the position when the combination of selling prices for production is not an advantage over the dry gas producers.

It is possible that the Canadian producers will benefit more from the ability to export natural gas because the Canadian market is so small, that export capacity would enable the industry to grow relatively more than is the case in the United States.

The Canadian industry also sends gas down to the Gulf Coast for exporting, and so can benefit from the growing export capacity there as well. This particular investment idea is more complicated than some of the others I follow.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here