I believe Chesapeake Energy (NASDAQ:CHK) to be a little bit of a diamond in the rough, as it were. Not because they’re necessarily rough, they aren’t, but because the natural gas market is depressed at the moment. Chesapeake has great leadership, and is looking for a chance to shine.

They’re positioned well for it. They’ve consolidated their land holdings into some of the best, highest margin, most sought after pieces of real estate in the natural gas market. And more than that, they’re very close to distribution hubs.

The company’s stock prices are a bit down at the moment due to NG pricing, but that’s likely just a temporary scenario. As you’ll see by the end, I believe it’s an opportune time for the patient investor to grab up this future dividend star.

Company Overview

Chesapeake Energy Corporation is focused on exploration and production of natural gas resources in the United States. It is now almost entirely a pure-play natural gas company, with 1Q23 production of oil at only 54 MBOD. Founded in 1989, it is headquartered in Oklahoma City, Oklahoma.

The company possesses stakes in several natural gas resource plays:

- In the Marcellus Shale situated in the northern Appalachian Basin in Pennsylvania.

- The Haynesville/Bossier Shales located in northwestern Louisiana.

- A small position in the in the Eagle Ford Shale in South Texas.

Investors should note that in 2020 Chesapeake Energy actually filed for Chapter 11 bankruptcy due to the company’s legacy debt and contractual obligations. The company entered into a Restructuring Support Agreement to eliminate approximately $7 billion of debt. The company continued operating as usual throughout the restructuring process.

In February of 2021, Chesapeake successfully concluded its restructuring process and emerged from Chapter 11, satisfying all conditions of the plan of reorganization.

Operations

Chesapeake has large positions in some of the top U.S. shale plays for gas. The company does drilling, completion, and production operations, including horizontal drilling, hydraulic fracturing, and actual production of the commodity.

The company’s interest is almost exclusively natural gas and investors should note that the performance of the company is dependent on natural gas markets. The company operates in three premier shale plays in the Haynesville, Marcellus, and Eagle Ford Shales.

Marcellus Shale

One of the largest natural gas fields in the world, it’s only right that a natural gas giant like Chesapeake has a core position here and is one of the largest operators in the Marcellus Shale.

The formation is estimated to have enough gas to supply U.S. natural gas needs for hundreds of years. The company operates on average 5 active rigs and the Marcellus Shale makes up for 54% of the total company production.

Their gross margins here are 72.4% after all production, gathering, processing, and tax expenses. The Marcellus received only $118M of ~$500M total capex in Q1.

Haynesville Shale

The Haynesville Shale is a formation rich in natural gas and a premier gas play due to the close proximity to liquified natural gas export infrastructure. Chesapeake began developing natural gas here in 2008 and currently holds leases covering approximately 370,000 net acres. The company operates 7 active rigs and production in the Haynesville shale makes up 42% of total company production.

Their gross margins here are 62.9% after all production, gathering, processing, and tax expenses. Haynesville also garnered the biggest capex with $259M of ~$500M total in Q1.

Eagle Ford Shale

Investors should note that Chesapeake actually sold off most of their position in the Eagle Ford Shale to Wildfire Energy LLC and INEOS Energy this year.

This leaves Chesapeake with approximately 50,000 acres in the southwest portion of the play, which is the portion rich with natural gas. Production in the Eagle Ford Shale makes up for only 4% of total company production.

Their gross margins here are 59.6% after all production, gathering, processing, and tax expenses – at least prior to the sale.

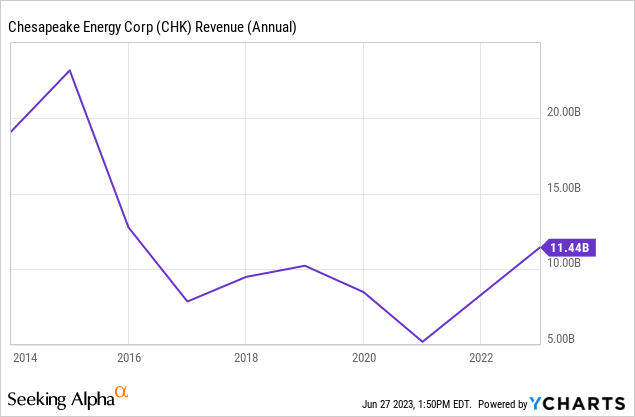

Revenue

Chesapeake’s revenue has never really been stable, even for the energy sector. We’ll continue to see some wide variations in revenue as the company solidifies its current holdings and navigates the potentially rough economic waters we now find ourselves in. This year they’re scheduled to drop to $4.2B, with $4.4B next year.

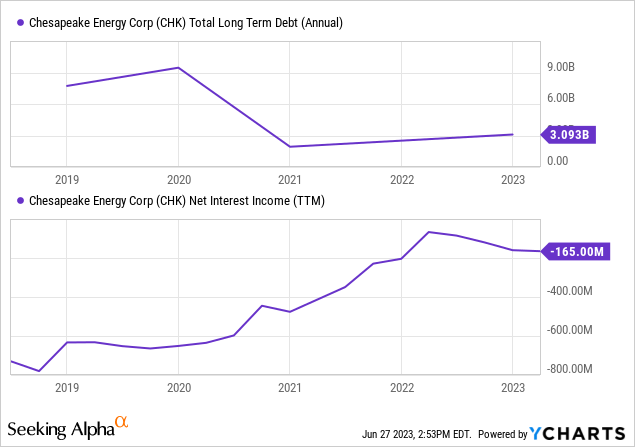

Debt

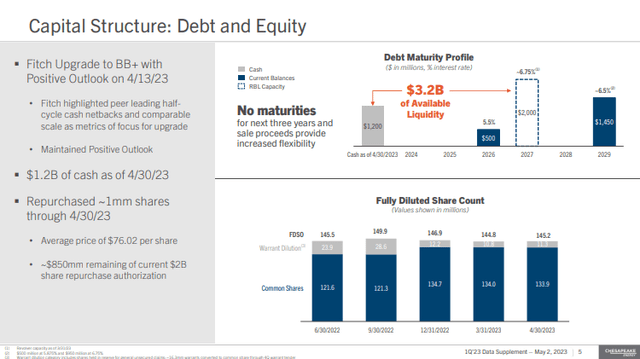

Since emerging from bankruptcy CHK has done a fair job of maintaining their debt levels with reasonable interest coverage (currently sporting a 36x ratio). They also have a great maturity schedule, giving them plenty of runway:

CHK Debt Maturity Profile (CHK 1Q23 Investor Presentation)

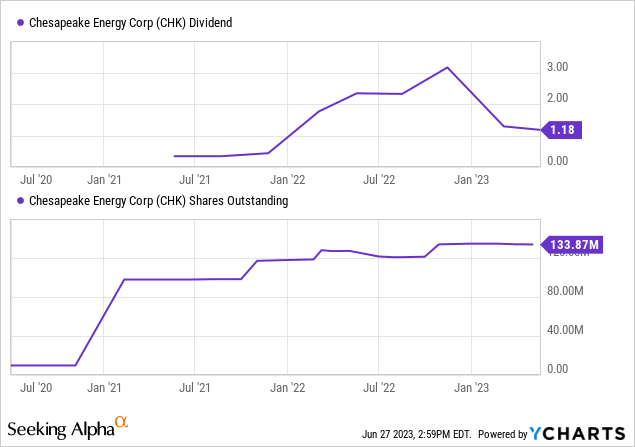

Return of Value to Shareholders

Paying special dividends since the beginning of 2022, the big question for investors is if they can continue paying them? The base dividend is fairly small, but specials are bringing 2023 up to around 5.7% based on the last dividends. Much less than 2022’s blowout year and not fantastically competitive in the upstream market – but there’s good news ahead. Read on. First, will they keep up the dividends in this market environment. They say they will. From the Q123 earnings transcript:

Zach Parham

Thanks for that color, Josh. Nick, maybe one for you. We’ve seen some of your E&P [ph] peers shift their cash return programs away from variable dividends to focus more on buybacks. Any thoughts on shifting away from the base dividend program in favor of more buybacks.

Nick Dell’Osso

We’ll continue to do what we’re doing right now, Zach. Our free cash flow, obviously, is coming down as we move through this year with lower prices. And so the variable dividends come down with that. We love having the buyback there to continue to use the cash we have to return cash to shareholders. We think it’s worked pretty well so far. We get a lot of varying feedback from investors with some investors really favoring the implied discipline of the dividend, balanced with the buyback. We’re — as I’ve said all along, we’re not dogmatic about any of this and we’ll continue to think about what makes most sense. We’ve liked what we’ve done so far. We think it makes sense to continue it but we’ll continue to monitor it. And if there’s some change in the future that makes sense, we would do it. Otherwise, I’d say we’ll keep doing what we’re doing.

They seem to be set on continuing the current variable and base structure, but with lower free cash flow investors will see lower returns. Now we also have to consider the lows currently in the NG market. Prices can go lower, but it’s unlikely. And the current contango in NG suggests a bullish 2024. Right now the Dec 2024 futures for Henry Hub are showing $4.19.

CHK clearly has the gross margins to support a decent dividend and considering the potential forward pricing of NG and the increases to CHK’s FCF, it’s looking like a great deal.

In this writer’s opinion, it’ll drop a little through the end of the year and then pick up as they bring more production online over time and move more into international export markets. When prices start to move bullishly again, that variable dividend will become stellar. I wouldn’t be surprised to see CHK moving into the 9%+ range with a combination of bullish NG pricing and share buybacks.

Valuation and Price Target

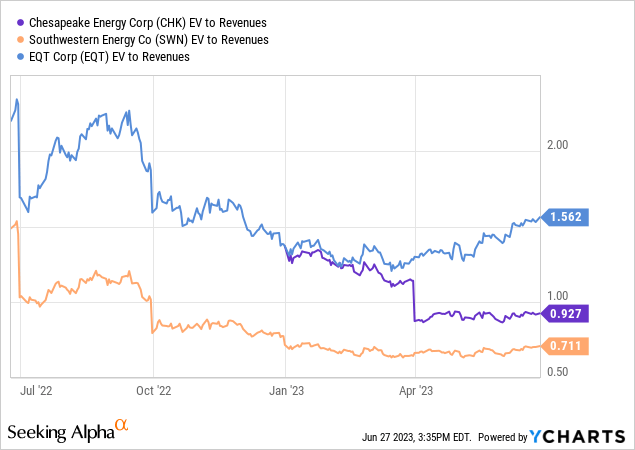

Compared to a few industry peers, Chesapeake is right in the lower range of EV/Revenue. And compared to itself, it is at its lowest values yet. Right now their Price/Book is very close to 1, indicating a fair valuation. Price/Sales and Price/Cash Flow are both a thumbs up from me and indicate fair to mild undervaluation.

Overall I’d have to believe CHK is probably fairly valued for its current state, but undervalued on a forward basis when we consider when the future of NG pricing has for us. If it materializes, of course. And I think that’s what a lot of investors are doing here – taking a “wait and see” approach.

Earnings Call Analysis

This call seemed to be a routine earnings call where the company discussed its financial and operating results for the quarter with the participants and answered any questions they had. There were no major announcements or surprises during the call.

The company has recently received a Fitch credit rating upgrade to BB+ with a positive outlook. Overall, the company seems to be taking a cautious approach in the current environment, focusing on prudent decision-making that will maintain productivity and financial flexibility while also monitoring market conditions and adjusting its plans accordingly.

Final Analysis

Chesapeake Energy Corporation looks to be back and better than ever after its bankruptcy in 2020. Chesapeake has always been primarily natural gas and after the bankruptcy and restructuring, the company is now almost a pure-play natural gas company.

What a lot of investors don’t know is that many of the company’s peers during the times of trouble were smelling blood and eagerly hoping to gobble up some of Chesapeake’s core positions.

This is because, although controversial during the time, Chesapeake went around gobbling up landowner rights and core positions all across the most prolific natural gas reserves and shale plays across Oklahoma and the rest of the country in the early and mid-2000s.

So investors should note that Chesapeake has rights to what is widely agreed upon in the industry as some of the very best gas reservoirs in the country.

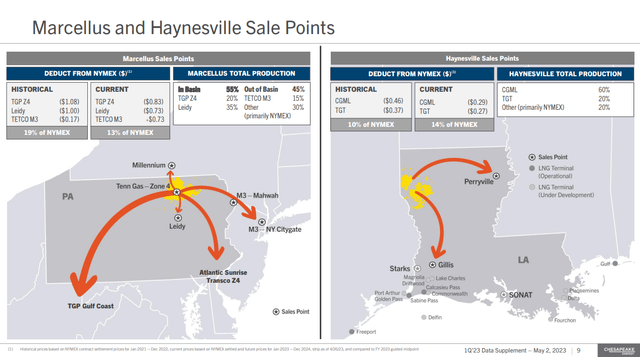

Additionally, after the restructuring, Chesapeake was smart and went purely for what they do best – natural gas. Literally, ALL of Chesapeake’s core positions are located very close to the most extensive LNG export infrastructure in the world, ensuring the company should almost always be a leader amongst its peers when it comes to breakeven pricing and will continue to be a leader in LNG exports. Check the map:

CHK Sale Points (CHK 1Q23 Investor Presentation)

Natural gas pricing is currently at where most traders would consider a bottomed-out low right now, and demand is expected to increase in the coming months and years – particularly for exports. This bodes well for the company and investors should certainly be excited about the future of Chesapeake. It’s also notable that there’s currently a contango in natural gas prices.

It’s no secret that there are a lot of economic factors pointing to a possible recession in our country. If the country were to go into a recession, we could likely expect demand for natural gas to decline a little bit – but not nearly as much as for oil.

Chesapeake would likely be reasonably well shielded compared to its peers in the event of a recession because the company is gearing up for massive exports of its LNG products. Naturally, the company would take a hit with lowered natural gas prices, but exports shouldn’t drop too much just because of an American recession. Europe is consuming more and more natural gas and the U.S. is the one supplying it.

At the end of the day, the future performance of the company and the stock is going to come down to natural gas markets. I believe that Chesapeake has shown fiscal responsibility and has done a great job focusing its assets and production in the best possible areas it could. And I know that Chesapeake held on to their highly sought-after landowners’ mineral rights throughout the bankruptcy process.

Conclusion

Investors should rest comfortably with the direction of the company and concern themselves entirely with the natural gas market outlook. All indicators point to increased demand for natural gas in the coming months and years so it’s currently all-systems go for Chesapeake to thrive.

The company appears valued fairly for today, but undervalued on a forward basis when natural gas pricing is taken into account. This looks to me like a well-priced contender for a patient dividend investor’s account. I give it a buy.

About this article:

When I research stocks, I start with a “bird’s eye view” of the target company. Many of the things I went through in this article are what I’ll look at first.

When this bird’s eye view is complete, I’ll decide if I want to avoid the company for the time being or if it’s a potential candidate for investment. This article that you are reading is the result of my bird’s eye view examination.

It is designed to be an overall, high-level view of the company that you can read to determine if this company is something that you might consider as a candidate for investment. It is not possible to report everything about a company in the space of a single article, nor is it possible for me as an author to learn every detail about a company in the amount of time allotted to write an article.

You should not take my final conclusion on the company as your sole recommendation for investment, and you should conduct further in-depth research on your own to come to your final conclusions.

As a result of this, my “buy” recommendations come with an asterisk. And that asterisk is that this is only a high-level examination, and in-depth research that can take many hours, or days, of your time is still required. This is why my articles are short and to the point, with no fluff or filler. Just the facts that you need to know to move forward.

Read the full article here