A Quick Take On CSP Inc.

CSP Inc. (NASDAQ:CSPI) provides a wide range of managed IT services, security software and related IT consulting services.

The firm has produced profitable growth in recent quarters and has launched its ARIA security software product, which may drive growth in the period ahead.

Investors with a risk-on perspective may wish to consider a Buy of CSPI at around $24.80 per share on the company’s growth prospects.

CSPI Overview And Market

Lowell, Massachusetts-based CSP Inc. was founded in 1968 and operates in two segments, Technology Solutions and High Performance Products.

The Technology Solutions segment provides a wide range of value-added reseller products and services, professional IT consulting services and managed IT services.

The High Performance Products segment offers its ARIA Software-Defined Security solution, Myricom network adapters and products for digital signal processing applications in defense environments.

The firm is headed by President and Chief Executive Officer Victor Dellovo, who has been with the firm since 2003 and, prior to that, was President of Technisource Hardware.

CSP acquires customers through its direct sales and marketing efforts as well as through bidding processes.

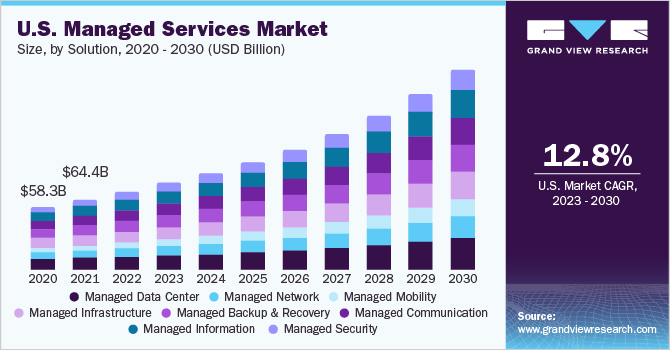

According to a 2023 market research report by Grand View Research, the global market for managed IT services was estimated at $267 billion in 2022 and is forecasted to reach $741 billion by 2030.

This represents a forecast CAGR (Compound Annual Growth Rate) of 13.6% from 2023 to 2030.

The main drivers for this expected growth are the difficulty in finding qualified persons to handle the increasing complexity in systems design and administration.

Also, the chart below shows the historical and projected future growth prospects for the managed services market in the U.S.:

Grand View Research

The firm also operates in software security and other hardware markets.

CSPI’s Recent Financial Trends

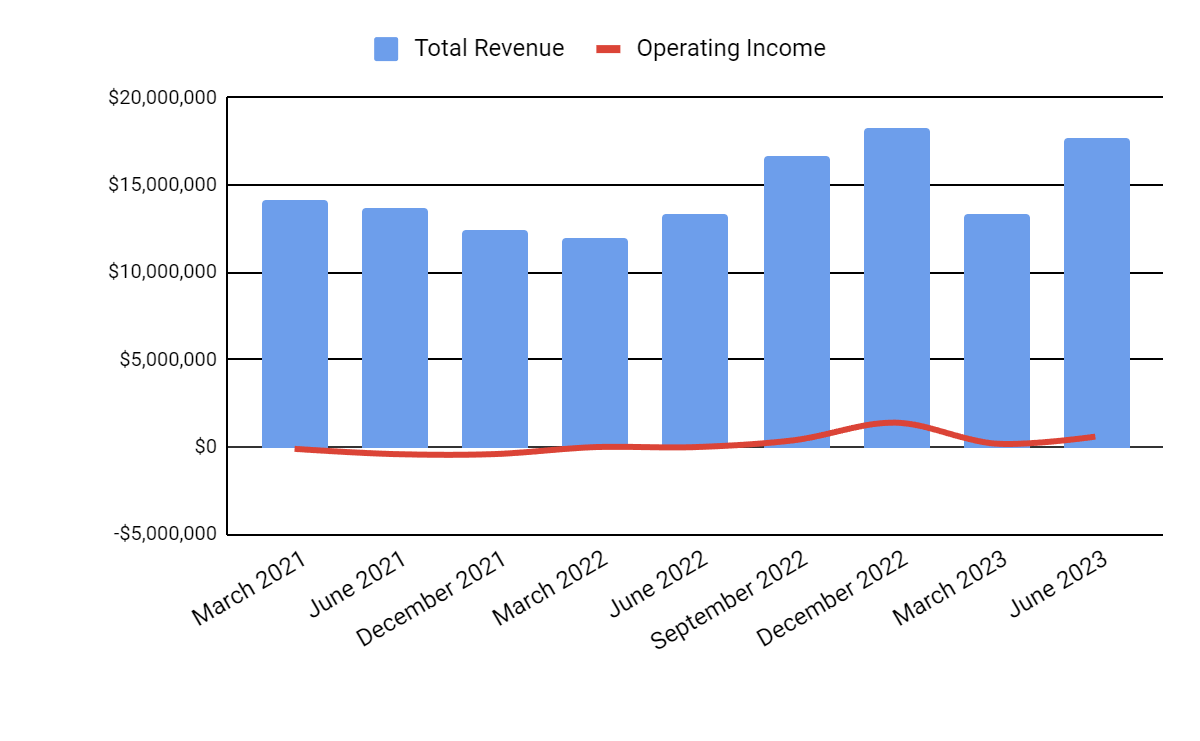

Total revenue by quarter (blue columns) has continued to grow, although unevenly; Operating income by quarter (red line) has remained positive in recent quarters:

Seeking Alpha

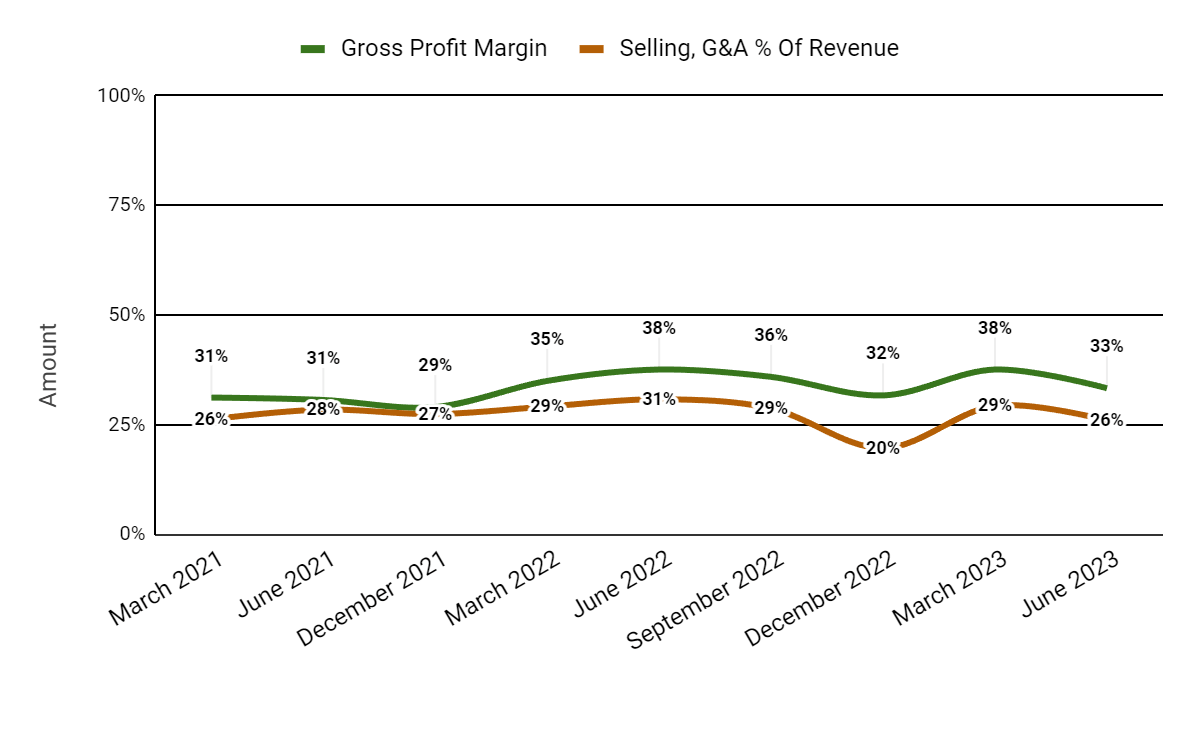

Gross profit margin by quarter (green line) has fluctuated without a discernible trend; Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have trended lower more recently, indicating increasing efficiency in this regard:

Seeking Alpha

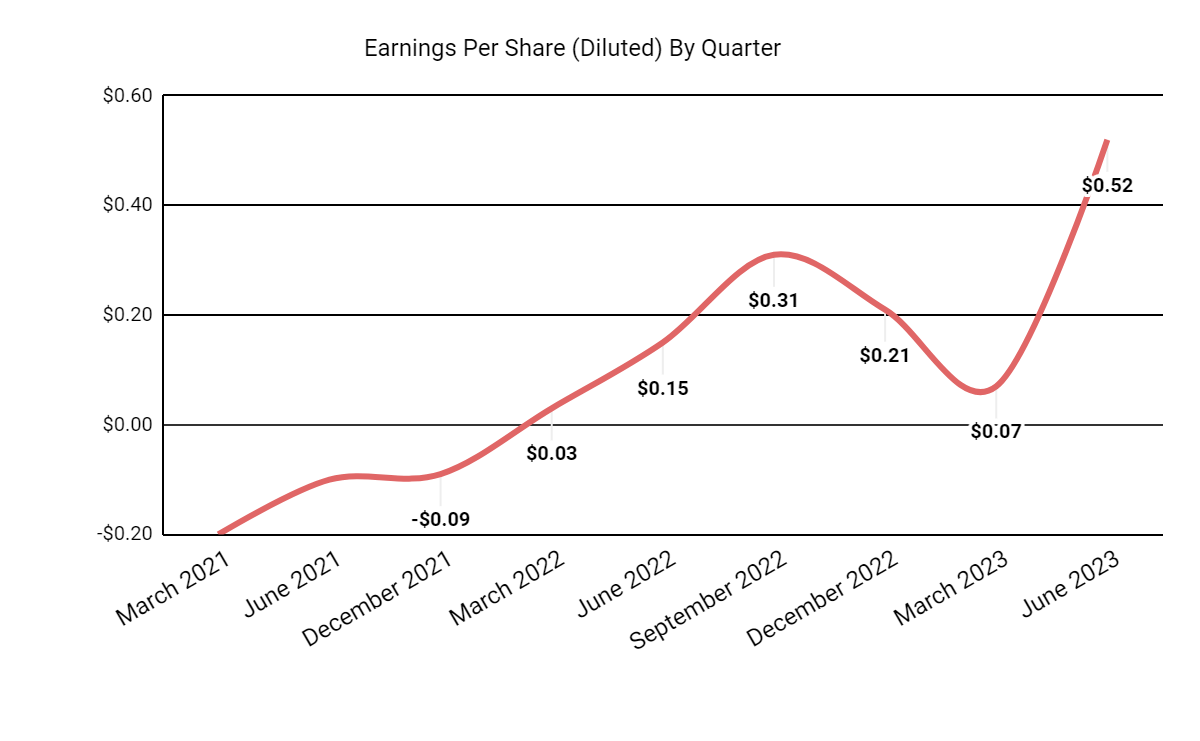

Earnings per share (Diluted) have turned sharply higher in the most recent quarter:

Seeking Alpha

(All data in the above charts is GAAP.)

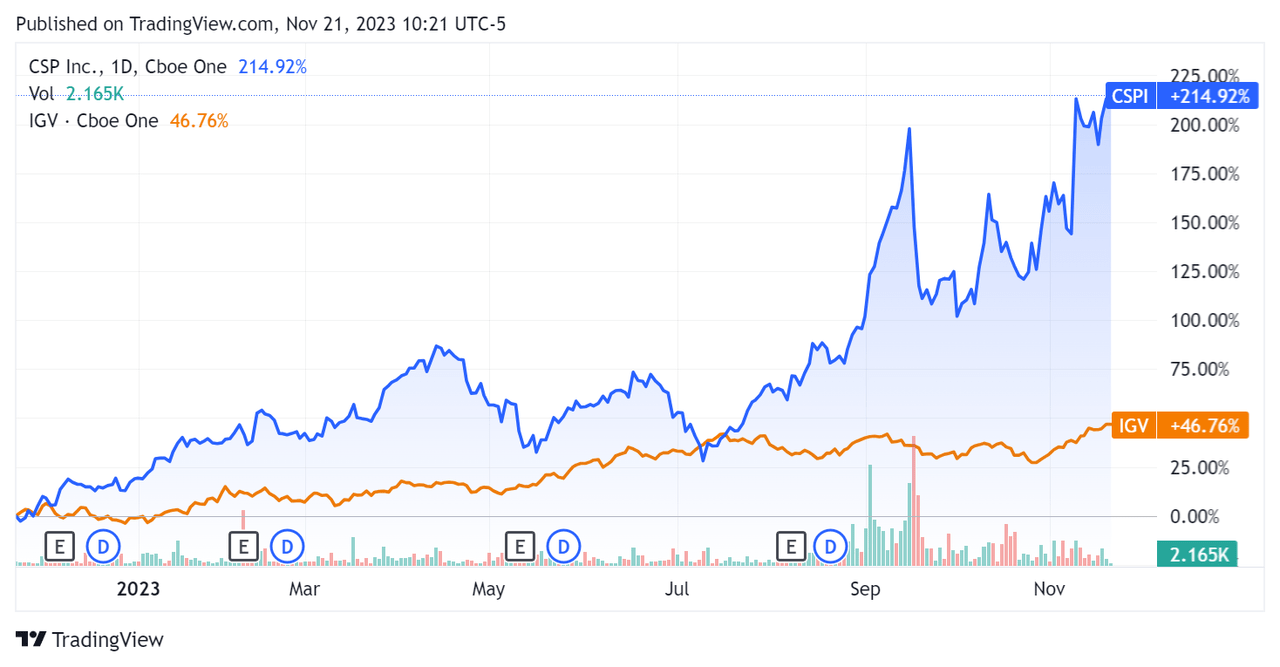

In the past 12 months, CSPI’s stock price has risen 214.92% vs. that of the iShares Expanded Technology-Software ETF’s (IGV) gain of 46.76%:

Seeking Alpha

For balance sheet results, the firm ended the quarter with $16.2 million in cash and equivalents and $1.7 million in total debt, all of which was categorized as short-term.

Over the trailing twelve months, free cash used was ($2.7 million), during which capital expenditures were $0.2 million. The company paid $1.1 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For CSPI

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure (Trailing Twelve Months) |

Amount |

|

Enterprise Value / Sales |

1.5 |

|

Enterprise Value / EBITDA |

34.3 |

|

Price / Sales |

1.6 |

|

Revenue Growth Rate |

38.4% |

|

Net Income Margin |

7.9% |

|

EBITDA % |

4.4% |

|

Market Capitalization |

$113,460,000 |

|

Enterprise Value |

$99,610,000 |

|

Operating Cash Flow |

-$2,490,000 |

|

Earnings Per Share (Fully Diluted) |

$1.11 |

|

Free Cash Flow Per Share |

-$0.64 |

|

R&D / Revenue |

5.0% |

(Source – Seeking Alpha.)

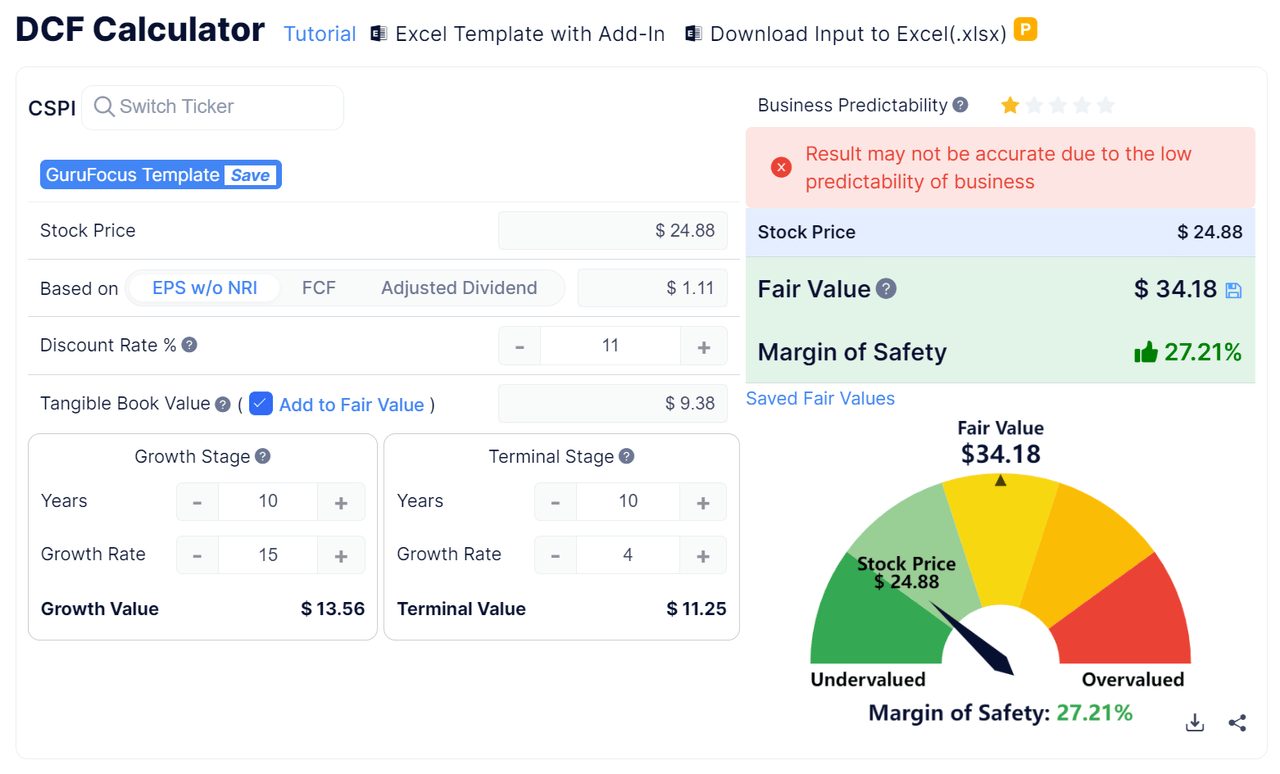

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

GuruFocus

Based on the DCF, the firm’s shares would be valued at approximately $34.18 versus the current price of $24.88, indicating they are potentially currently undervalued.

CSPI’s most recent unadjusted Rule of 40 calculation was 41.8% as of FQ3 2023’s results, so the firm has performed well in this regard, per the table below:

|

Rule of 40 Performance (Unadjusted) |

FQ3 2023 |

|

Revenue Growth % |

38.4% |

|

Operating Margin |

3.4% |

|

Total |

41.8% |

(Source – Seeking Alpha.)

Commentary On CSPI

In its last earnings call (Source – Seeking Alpha), covering FQ3 2023’s results, management’s prepared remarks highlighted “continued momentum” for its business as revenue growth was driven by the strong performance of its Technology Solutions business segment.

The company continued to work down its backlog, which had risen due to supply chain bottlenecks. Notably, the firm hasn’t “lost a single order” during this period of delays.

CSP also recently launched its ARIA Zero Trust PROTECT [AZT], and given the early industry feedback, management believes this system “will be a major growth driver” for its High Performance Products segment into 2024.

Analysts asked leadership about the potential for AZT product partnerships, capital allocation strategy and international expansion opportunities.

Management responded that it is currently looking to build its customer base through internal efforts and consider partnerships later on.

The firm has been focused on investing in the AZT product and launch, so capital allocation has aimed at success with that process.

On international expansion in the managed service provider space, the company is seeking to work with partners that are focused on its offering, not just adding a line item to their catalog.

Total revenue for FQ3 2023 rose by 33.1% YoY, while gross profit margin dipped by 4.3%.

Selling and G&A expenses as a percentage of revenue fell by 4.8% year-over-year, a positive development, and operating income rose to $600,000 for the quarter.

CSP’s R&D / Revenue ratio was 5% for the last four quarters, which is materially lower than many technology firms of its size.

The company’s financial position is solid, with ample liquidity, little debt and a small amount of free cash burn in the last four quarters.

CSP’s Rule of 40 performance has been good, although it has been driven primarily by the company’s revenue growth rate.

Looking ahead, management is clearly focused on ramping up the AZT security software, which has the promise to produce initial growth signals as early as fiscal Q4 2023.

In the past twelve months, the firm’s EV/Sales valuation multiple has risen to nearly 4.5x its starting level, as the chart from Seeking Alpha shows below:

Seeking Alpha

While CSPI continues to work through hardware supply chain issues, its AZT security software looks to have the potential to drive the company’s future growth trajectory.

Risks to the company’s stock could include a slowing demand environment as customers closely watch every dollar spent, slowing sales cycles and the firm’s growth outlook in the near term.

Investors with a risk-on perspective may wish to consider a Buy of CSP Inc. stock at around $24.80 per share on the company’s growth prospects ahead.

Read the full article here