If you an income-focused investor, you have likely come across energy midstream companies (including master limited partnerships (“MLPs”)). These specialized companies generally transport oil and gas through pipelines, and they can offer some of the biggest and steadiest income payments in the market. However, before you invest in any of these companies, you need to understand the unique nuances and tax risks of the MLP structure, particularly with regards to account types (i.e. should you hold MLPs in your IRA, your taxable account, or neither). In this report, we share data on the top 10 midstream companies (including the top 5 MLPs), review Energy Transfer (an MLP) in particular (including its business, big yield, valuation and risks), and then conclude with our strong opinion on if (and where) your should even consider including Energy Transfer in your prudently-diversified big-yield investment portfolio.

Energy Transfer![]()

Overview: Energy Transfer (NYSE:ET)

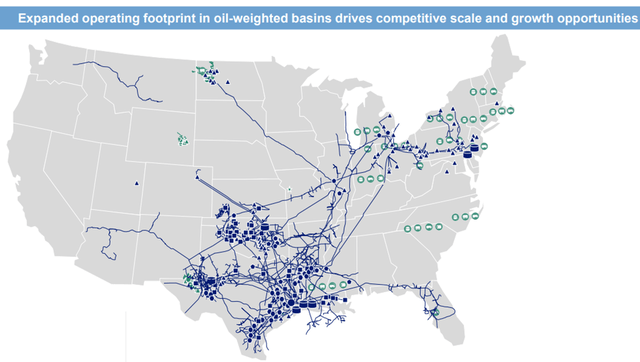

Energy Transfer is one of the largest and most diversified midstream energy companies in North America. It has more than 125,000 miles of pipelines and associated energy infrastructure in 44 states. It transports much of the oil and gas products that make modern life possible (including everything from the clothes you wear and the food you eat to the transportation you use).

Energy Transfer Investor Presentation

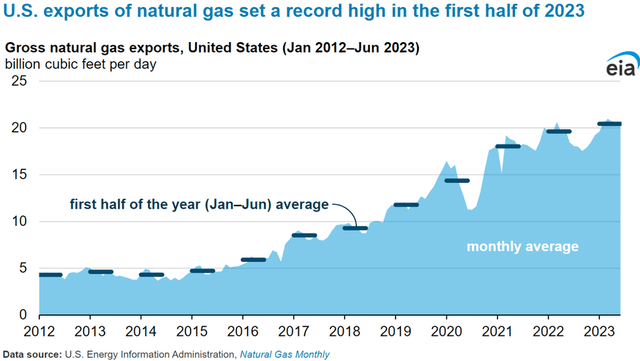

The business is particularly attractive (especially as compared to some other midstream companies) because it is diversified across multiple geographies and commodities, thereby giving it access to big customers. Further still, Energy Transfer is well positioned to benefit from growing natural gas exports.

Natural Gas Monthly

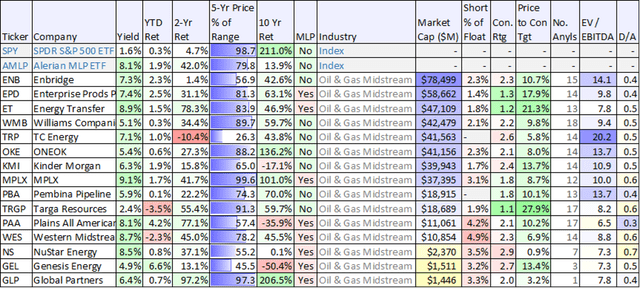

Top 10 Midstream Companies

Before going deeper into Energy Transfer, here is a quick look (for comparison and perspective) at some data points for a variety of the largest midstream companies, sorted by market cap.

data as of Fri 1/12/24 (StockRover)

(ENB) (EPD) (ET) (WMB) (TRP) (OKE) (KMI) (MPLX) (TRGP) (PBA) (WES) (PAA)

As you can see in, Energy Transfer is one of the largest midstream companies, and it has one of the lower valuations (arguably quite attractive, as we will discuss later in this report). Wall Street analysts also rate it a strong buy (1.0 = strong buy, 5.0 = strong sell).

Big Distribution Yield

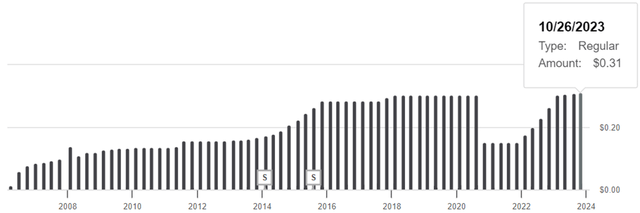

One of the main reasons many investors are attracted to Energy Transfer is its big distribution yield (currently ~9.0%). The company targets a 3% to 5% annual distribution growth rate, and recently announced another increase in the distribution to $0.3125 per unit.

Seeking Alpha

For the most recently reported quarter, total distributable cash flow was $2.0 billion, and the company had ~$1.0B in excess cash flows after distributions. Share (“unit”) repurchases are also an option, although the company has been more recently working on getting its leverage (debt) level down to the 4.0 to 4.5 target range. And on that front, the company has been making positive progress (in August, Energy Transfer’s senior unsecured credit rating was upgraded by S&P to BBB with a stable outlook).

Preferred Unit Distributions:

Also important to mention, Energy Transfer (or its subsidiary, Energy Transfer Operating, L.P.) has issued multiple series of preferred units, but they will be redeemed soon (as per this press release). Specifically, series C, D and E preferred units (listed on the NYSE under ticker symbols (ET.PR.C) (ET.PR.D) (ET.PR.E)) will be redeemed following the issuance of $3 billion of senior notes and $800 million of junior subordinated notes. We view this as a positive for the company (but not necessarily for the holders of the preferreds) considering the transactions will essentially allow the company to refinance outstanding debt (i.e. the preferred shares) at a lower rate.

DRIP Plan:

Also noteworthy, Energy Transfer offers a Distribution Reinvestment Plan, which can be an outstanding way for owners to reinvest their distributions. The plan allows owners to purchase additional common units by reinvesting all or a portion of the quarterly cash distributions paid. Importantly, additional units purchased through the plan will be sold at a discount ranging from 0% to 5% (unfortunately it’s currently set at 0.0%) but investors do not pay any service fees, brokerage trading fees or other charges (this is a good thing).

Valuation:

From a valuation standpoint, Energy Transfer appears very attractive. Specifically, the company currently has one of the lowest EV/EBITDA valuations (see our earlier midstream data table) and one of the best Wall Street analyst ratings (again, see our earlier table, it’s rated “1.2” or “strong buy”). However, the units have been a bit chronically undervalued over time. Possible reasons for the low valuation include the risks of converting from an MLP to a C-Corp (more on this later) and the risk of more pricey acquisitions (the company has a history of this). However, the upside of the low valuation is that the distribution yield is quite high (attractive).

Master Limited Partnership Risks (“MLP”):

Energy Transfer is not a stock. As explained by the company:

“Energy Transfer is a publicly traded master limited partnership. Unitholders are limited partners in the Partnership and receive cash distributions. A partnership generally is not subject to federal or state income tax. However, the annual income, gains, losses, deductions, and credits of the Partnership flow through to the Unitholders, who are required to report their allocated share of these amounts on their individual tax returns as though the Unitholder had received these items directly.”

This MLP structure creates a few critically important nuances for investors to be aware of. For starters, you won’t receive the typical 1099 at tax time, instead you’ll receive a K-1 statement. And as the company explains:

“Energy Transfer will not pay any federal income tax. This allows for a higher potential cash flow payout to unitholders. Instead, each unitholder will be required to report on his or her income tax return his or her share of our income, gains, losses, and deductions without regard to whether corresponding cash distributions are received. As a result, a unitholder’s share of taxable income, and possibly the income tax payable by the unithholder with respect to that income, may exceed the cash actually distributed to the unitholder. Since MLPs generally pay more cash distributions than the amount of taxable income allocated, the tax basis of the unitholder is decreased by the difference between total cash received and taxable income reported. Cash distributions will become taxable if the unitholders’s cost basis is reduced to zero.”

MLPs and Individual Retirement Accounts:

Technically, you can own an MLP in your retirement account (e.g. Traditional or Roth IRAs and 401Ks), but according to the Energy Infrastructure Council (“EIC”) there are some special considerations you need to keep in mind:

“First, remember that one reason many people buy MLPs is for the tax advantages — the tax-deferred distribution and the ability to offset taxable income passed through from the MLP with depreciation and other deductions. In a retirement account, however, the income is already tax-deferred, so the tax benefits of an MLP are, in a sense, ‘wasted.’”

And very importantly, holding an MLP in a retirement account can end up resulting in you owing income tax, through the concept of “Unrelated Business Tax income” (“UBTI”). According to the EIC:

“As a partner in the MLP, the IRA or other account is considered to be “earning” its share of the MLP’s business income. The MLP’s business is not related to the retirement account’s tax-exempt purpose; therefore the IRA’s share of the MLP’s income is treated as UBTI and is taxed accordingly.”

The bottom line here is that there are important nuances to holding MLPs in a retirement account, and depending on your own personal situation, it may or may not make sense to do so. Also worth mentioning, some brokerages won’t even allow you to own an MLP in a tax-advantaged retirement account (e.g. IRA, 401K).

Energy Transfer May Switch to a C-Corp:

Another big risk factor investors should consider is that Energy Transfer may switch from the MLP structure to a C-Corp as other MLPs have been doing in the relatively recent past. And the big problem is that MLP conversions are often treated as a taxable sale for unit holders. This means you own tax on your adjusted cost basis, and this can be a very large amount (recall, MLP partners often have reported taxable income greater than the size of the distributions they receive thereby reducing their cost basis significantly over time).

And according to a November 2023 note from Morningstar Strategist, Stephen Ellis:

“Energy Transfer seems to be considering a C-Corporation conversion, or C-Corp, alternative more seriously than it has in the past as an alternative to buybacks. Co-CEO Thomas Long said he thinks the C-Corp currency makes a lot of sense, and the company is spending considerable time evaluating it. This shift seems to suggest that Energy Transfer management may have thought the stock would rerate higher with the increased yield (currently 9%), but in the absence of that, it may consider a C-Corp conversion to address the long-standing EBITDA multiple discount versus peers.”

Morningstar

The possibility of a C-Corp conversion for Energy Transfer is a big risk factor, especially if you have owned your MLP units for an extended period of time.

Environmental Risks:

As mentioned, Energy Transfer transfers much of the oil and gas products that make modern life possible. However, it faces constant pressures and risks from environmentalists and regulators. For example, it has a long-running legal battle on its Dakota Access pipeline that has significantly changed the course of business operations. Regulatory risks are another factor investors should keep in mind.

Conclusion: A Ranked Big-Yield Opportunity

Energy Transfer is an extremely attractive business due to the steady high cash flows from its pipeline operations and its well covered (and very large) quarterly distribution (which continues to grow). And the units currently trade at a very attractive valuation, although the low price is likely also a reflection of the risks (such as the challenges for some investors in owning MLPs and the potential negative tax impacts if the company converts from an MLP to a C-Corporation).

In our view, investing in Energy Transfer comes down to your own individual situation and goals. If you can handle the unique nuances of the business (and the MLP structure), we believe it can be an extremely attractive addition to a prudently diversified high-income portfolio. In fact, we just ranked Energy Transfer (as an honorable mention) in our latest Top 10 Big Yields report, ahead of RQI at #8 (read report) and behind Ares at #6 (read report).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here