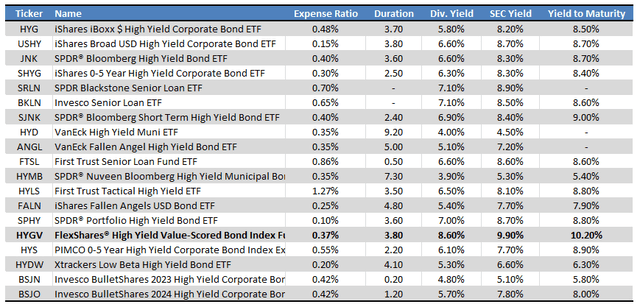

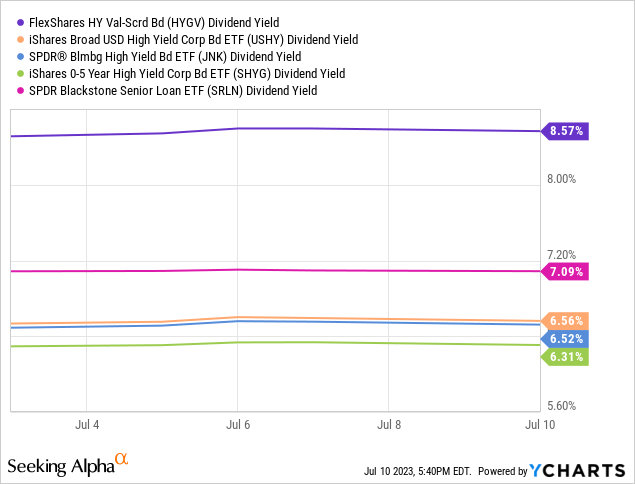

While making a table on some of the larger high-yield corporate bond ETFs, I noticed that the FlexShares High Yield Value-Scored Bond Index Fund ETF (NYSEARCA:HYGV), a little-known fund, has a particularly strong 8.6% dividend yield:

Fund Filings – Chart by author

Considering the above, I thought to have a closer look at HYGV, and to share my findings with readers.

HYGV sports an incredibly strong yield, and does OK in most other relevant metrics, including risk, duration, total returns, and dividend growth. In my opinion the fund is a buy, and particularly appropriate for more bullish long-term income investors.

HYGV – Basics

- Investment Manager: FlexShares

- Underlying Index: Northern Trust High Yield Value-Scored US Corporate Bond Index

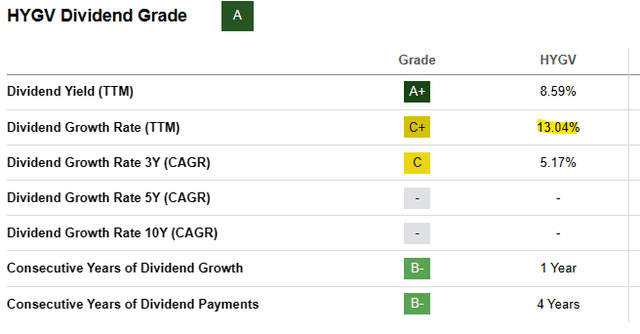

- Dividend Yield: 8.59%

- Expense Ratio: 0.37%

HYGV – Overview and Analysis

Strategy and Holdings

HYGV is a high-yield corporate bond ETF. It is technically an index fund, tracking the Northern Trust High Yield Value-Scored US Corporate Bond Index. This is a be-spoke index, and so, in practice, the fund functions more like an actively-managed or smart beta fund.

The index first selects all eligible securities, based on a basic set of inclusion criteria centered on liquidity, size, etc. The index then invests in the cheapest of these, based on their prices and spreads, subject to strict credit and liquidity screens. The process is quite thorough, although the details are proprietary.

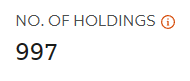

HYGV’s underlying index aims for adequate diversification, resulting in a reasonably well-diversified fund, with over 1,000 holdings from most relevant industry segments.

HYGV HYGV

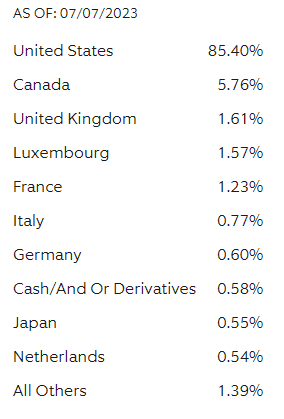

The fund focuses on U.S. bonds, but does include smaller investments bonds from other countries.

HYGV

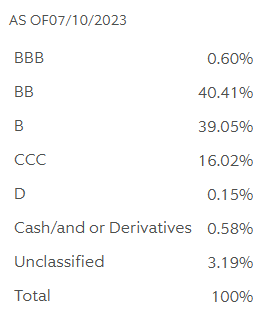

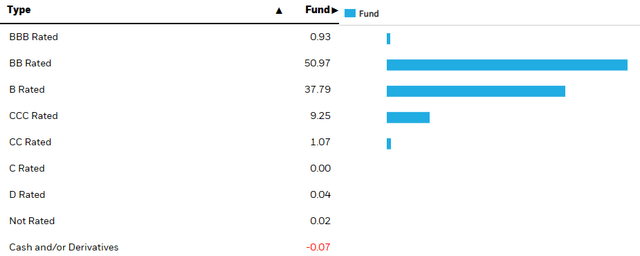

The fund focuses on securities with above-average value and spreads which, in practice, means weaker credit ratings. HYGV focuses on securities rated BB and B, as do most other high-yield corporate bond ETFs, but the fund has lower BB allocations than average, and higher CCC weights too. Credit ratings are as follows.

HYGV

For reference, credit ratings for the iShares iBoxx $ High Yield Corporate Bond ETF (HYG), the largest fund in this space.

HYG

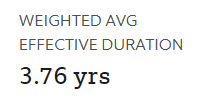

Finally, the fund sports a weighted average duration of 3.8. It is quite a bit lower than average for a bond fund, and very slightly lower than average for a high-yield corporate bond fund.

HYGV

Besides the above, not much else stands out about the fund’s strategy or holdings. It is a simple high-yield corporate bond ETF, with slightly weaker credit ratings than average.

Dividends and Dividend Growth

HYGV invests in high-yield corporate bonds, which tend to carry strong yields, higher than those of most bonds and bond sub-asset classes. This is the case for the fund as well, as expected.

The fund further focuses on bonds with value characteristics, meaning low prices and above-average spreads. The result should be a yield higher than average for a high-yield corporate bond fund, as is indeed the case.

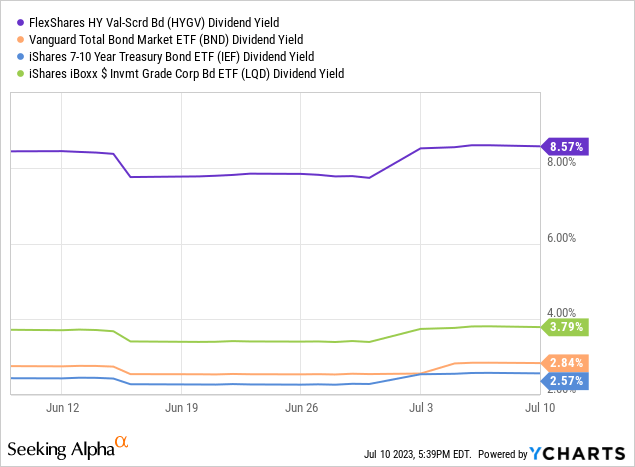

Importantly, HYGV’s dividends are higher than those of basically all of its peers, across all relevant dividend metrics. These include 12m dividend yields, SEC yields, and yield to maturity.

Fund Filings – Chart by author

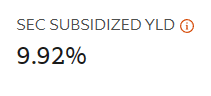

HYGV’s strong 9.9% SEC yield is a significant benefit for the fund and its shareholders, and the fund’s key advantage relative to peers.

HYGV’s dividends have seen very healthy growth these past twelve months too, courtesy of Fed hikes.

Seeking Alpha

Importantly, HYGV’s dividends should see strong growth moving forward as well. The fund’s underlying holdings currently generate around 9.9% in income, as per the fund’s SEC yield.

HYGV

As ETFs almost always distribute any and all income generated to shareholders as dividends, USIG’s yield should increase to around 9.9% in the coming years.

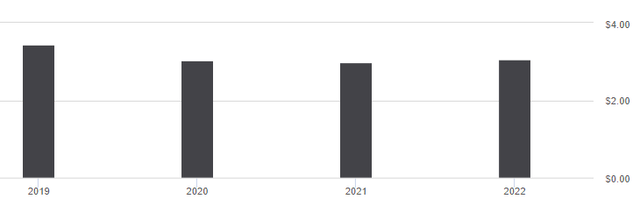

On a more negative note, HYGV’s dividends have declined since inception, by around 12% since 2019. The decline was almost entirely due to declining rates and spreads from 2019 to 2021, and has not persisted in the current rising rates environment.

HYGV

In my opinion, and taking into consideration recent Fed hikes, HYGV’s dividend growth track-record / expectations thereof is reasonably good. Rates did decline in prior years, but this occurred when the Federal Reserve was slashing rates, which is not currently the case. HYGV would, off course, almost certainly see declining dividends it the Fed were to slash interest rates in the coming months. Although this does not seem terribly likely, it is definitely an important consideration.

Risk and Losses During Downturns

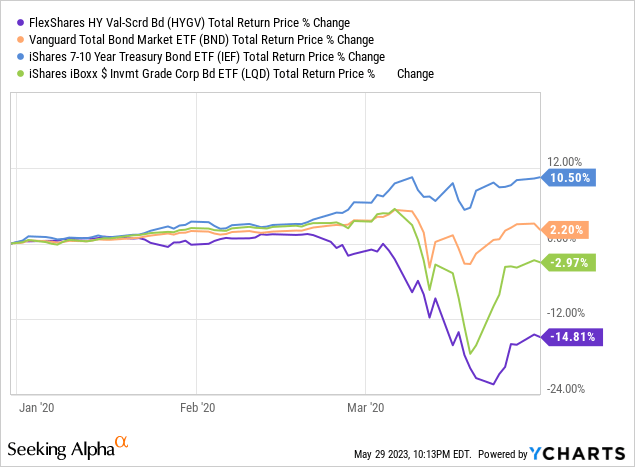

HYGV focuses on high-yield corporate bonds, which are riskier than average bonds, with higher default rates. Expect higher losses than those of most bond funds during downturns, as was the case in 1Q2020.

Data by YCharts

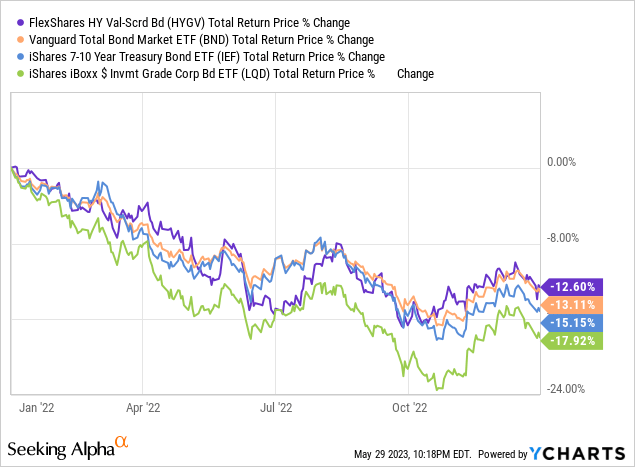

On a more positive note, HYGV’s duration is lower than average, which should result in below-average losses when interest rates increase. This was the case in 2022, as expected.

Data by YCharts

HYGV focuses on high-yield corporate bonds with cheap prices and above-average spreads which, in practice, means weak credit ratings. At the same time, the fund’s holdings are subject to strict credit and liquidity screens. The end result should be above-average risk and losses relative to high-yield peers during downturns, although much will depend on specifics. Sufficiently strict screens might completely counteract the weak credit ratings, for instance.

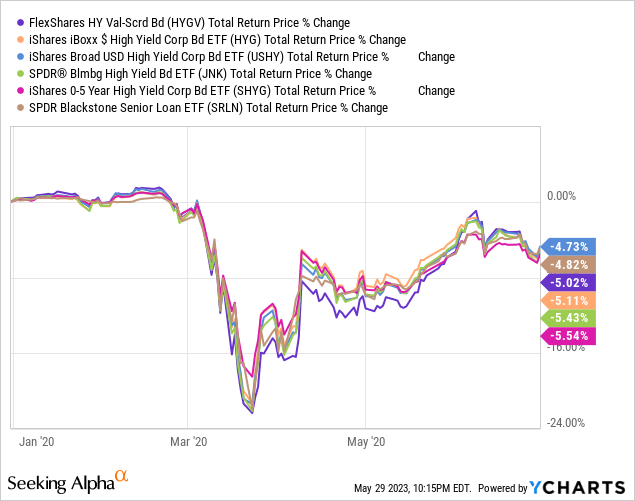

HYGV itself seems slightly riskier than the average high-yield corporate bond, but barely so. HYGV saw higher losses than average during 1Q2020, but these were very short-lived, and could have been the result of volatility. By 2Q2020 the fund was performing in-line with its peers, even slightly better than average.

Data by YCharts

In my opinion, and considering the above, HYGV is slightly riskier than the average high-yield corporate bond ETF. Risks are more than manageable, and appropriate for most income investors. Some more conservative investors might disagree, and might prefer safer, higher-quality funds focusing on t-bills and the like.

Performance Track-Record

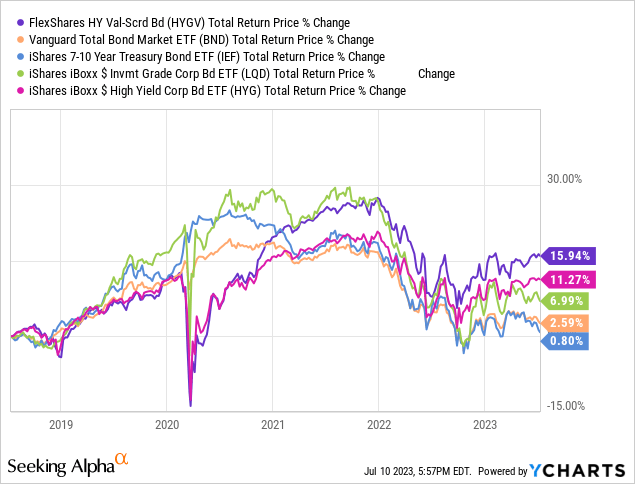

HYGV’s performance track-record is reasonably good, with the fund outperforming most bonds and bond sub-asset classes since inception.

Outperformance relative to broader high-yield corporate bond funds was due to HYGV’s higher yield, and strong capital gains as markets recovered from the coronavirus pandemic from late 2020 to early 2022. Outperformance relative to other bond sub-asset classes was due to the fund’s comparatively low duration, plus aggressive Fed hikes. I did not see any periods of significant, sustained underperformance.

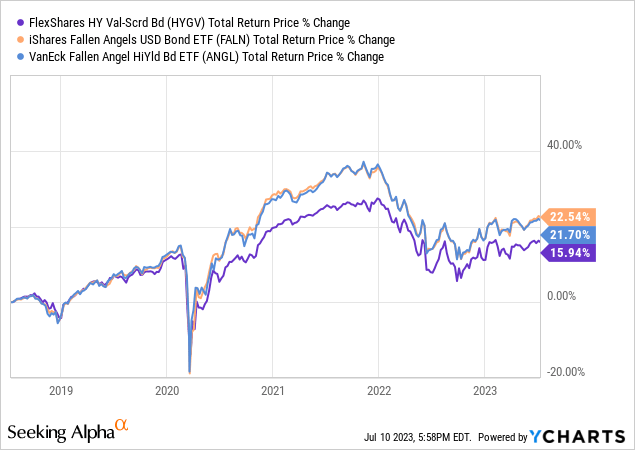

On a slightly more negative note, HYGV has underperformed relative to funds focusing on fallen angels, bonds downgraded from investment-grade to non-investment grade credit ratings. Broad high-yield corporate bond funds tend to underperform those focused on fallen angels, as is the case for HYGV.

In my opinion, HYGV’s overall performance track-record is quite good, although not outstanding. Fallen angels do have stronger performance, and tend to be great investment opportunities. I last covered fallen angels here.

Conclusion

HYGV sports a strong 9.9% SEC yield, higher than that of basically all high-yield corporate bond ETFs. HYGV is a strong investment opportunity, and a buy.

Read the full article here