The Japanese stock market is having itself a hot minute. The Nikkei 225 index, a benchmark for Japanese equities, is up nearly 30 percent so far this year, a standout performance among global markets and a sharp contrast to Asia’s other large economy, China, where stocks have been limping along in negative territory and getting little in the way of love from foreign investors.

Long a byword for chronic economic sluggishness, Japan is back on the radar screen. Is there a strategic case to make here? A word or two of caution is in order, we believe.

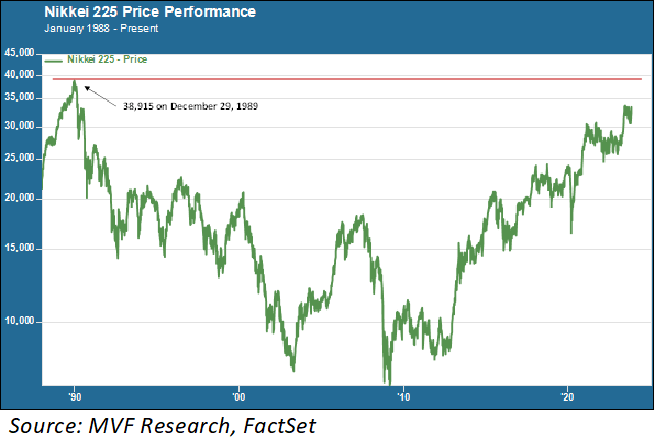

33 Years And Counting

Those of us with a sufficiently long institutional memory know that Japan is the asterisk tacked onto the mantra that stocks go up in the long term. The Nikkei 225 reached an all-time peak of 38,915 on the last trading day of the year in 1989.

Yes, the year that saw the fall of the Berlin Wall, Czechoslovakia’s Velvet Revolution and the birth of Taylor Swift, among other seismic world events, was also the last time the phrase “Japanese stocks closed at a record high” was ever uttered.

The Nikkei 225 today sits at 33,585. That is still around 14 percent below the 1989 record high, but it’s tantalizingly close, considering where the index has been for much of the intervening period, as the above chart shows.

Foreign investors have been a big source of the market’s upward trend this year. Last week, in the wake of a broad global rally on the back of positive sentiment about the Fed and interest rates, Japanese stocks attracted some $7.4 billion from international buyers.

Last month, the Wall Street Journal called Japan “the most exciting equity market in the world.” Warren Buffett has been a fan of late. Is there enough juice left for a final surge to bridge the 14 percent deficit and set a new record high?

Going Its Own Way

We are not going to make bets on short-term prospects for the Nikkei – that’s not what we do. But when we consider the strategic case for a long-term position in Japanese equities, we do not see much evidence to support such a move.

It is true that, after many years in which the economy flirted with chronic deflation, consumer prices have risen in the past couple years.

The national consumer price index currently sits around 2.7 percent – low in comparison to recent inflation levels in Europe and North America, but much higher than the levels of the previous decade when it struggled to stay above zero.

But at the same time that inflation is above trend – and above the Bank of Japan’s target of two percent – the economy is stagnating. Real GDP growth for the third quarter fell by 2.1 percent, a larger decline than expected.

Consumer spending is weak, as average domestic wages have not kept up with higher inflation. Capital investment by businesses was also negative.

The outlook for improvement in key areas like consumer spending is fairly muted. Japan risks transitioning from one kind of malady – deflation – to another – that old 1970s-era ball and chain of stagflation.

The government recently announced a proposed fiscal stimulus program that could potentially run to about three percent of the country’s total GDP. That might or might not work – stimulus efforts in the past have had decidedly mixed results.

But it comes at a very awkward time, because monetary policy has been delicately trying to go in the other direction – tightening (i.e., anti-stimulus) after years and years of one of the most aggressive monetary easing programs ever pursued by a central bank.

In addition to being the sole remaining country with negative benchmark interest rates, the Bank of Japan exerts pressure on long-term maturities through a policy of yield curve control.

It is trying to loosen this control, though the BoJ’s opaque pronouncements on the subject have tended to leave investors more confused than enlightened. Fiscal stimulus and a stagnating economy make the BoJ’s job even harder than it already was.

Japan has arguably done a more or less respectable job with its economic policies, going back to the “Abenomics” era of the early 2010s, in fighting against some deep-seated long-term problems, not the least of which is the demographic challenge of a declining working-age population (along with the intractable cultural resistance to increased immigration to offset demographic decline).

But the problems are not going away any time soon. At some point, we imagine the Japanese stock market will claw its way back to that 1989 high point. But for long-term portfolio allocation, we remain unconvinced.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here