Currently I am covering the biggest airplane manufacturers in the world. I am also covering various airlines and lessors that are the customers for these jets and I cover the big suppliers including the biggest airplane manufactures in the world, namely GE (GE), CFM (partnership between Safran (OTCPK:SAFRF) and GE) and Pratt & Whitney which is part of RTX Corporation (RTX). With the addition of Rolls-Royce (OTCPK:RYCEF, OTCPK:RYCEY), I am completing the coverage of engine manufacturers, meaning that going forward I will have all engine manufacturers covered.

What Does Rolls-Royce Do?

Rolls-Royce Motor Cars

If you hear Rolls-Royce, your mind most likely first goes to the car brand and later or not even to the manufacturer of airplane engines. That’s not odd, decades ago these companies were one. That changed in 1973. Two years earlier, in 1971, Rolls Royce had collapsed partially due to the development of the RB211 engine and was nationalized by the British government. Two years later, the car manufacturer was separated and sold while the other part of Rolls Royce focused on the aero engine. That part is now known as Rolls-Royce Holdings.

Rolls-Royce

Rolls-Royce consists of four reporting segments, namely Civil Aerospace, Defence, Power Systems and New Markets. All of these segments focus on products dedicated to power generation. Civil Aerospace focuses on aero engines for commercial and business jets, Defence focuses on military aero engines as well as powering naval vessels and submarines, while New Markets focuses on small modular reactors, urban air mobility and power solutions. What can be said is that the company focuses on in-demand products with end-market growth.

Rolls-Royce Has Faced Challenges

A Rolls-Royce Spectre, the car pictured above, costs around $400,000 while a single wide body airplane engine costs tens of millions of dollars. Nevertheless, the company has had continued challenges even after the de-merger of the car company. You could do an entire study on what the reason for that is, but the reality seems to be that the complexity of the engine architecture of Rolls-Royce makes a profitable OEM business where it sells engines at a profit to operators challenging, and while the company is among the biggest engine manufacturers in the world, the business has been challenged. The reason for that is two-fold or even three-fold I would say.

First, the company for a long time focused on harvesting the profits via its hourly service contracts. This TotalCare package allows for predictable maintenance costs for operators and simultaneously transferred the risk of shortcomings in operational reliability to Rolls Royce. What this essentially means is that a better engine would drive up revenues and profits, an unreliable engine would reduce the revenues and profits. This alignment would normally allow Rolls-Royce to make engines that would become better with each increment or each iteration or new engine family development. The reality was that cost overruns and reliability issues were detrimental to the ability to provide a strong competitive product. Rolls-Royce uses each time it faces difficulties, either due to macroeconomic factors or troubled engine development, to cut in costs and that goes at the expense of the competitive edge the company would like to generate. Furthermore, the company has for a long time focused so much on the profitable aftermarket revenues as its OEM product had challenges becoming profitable that the company would not be inclined to just sell engines to operators and that led to market share decline and almost in a position where it would not want to compete with other parties. It is not the case that the company cannot make its OEM sales profitable but it is also not a thick margin they will eventually generate.

Airbus

Finally, the company is primarily focused on wide body programs providing an engine option for the Boeing 787 (BA) and is the exclusive provider of Trent 7000 and Trent XWB engines for the Airbus A330neo and Airbus A350. Meanwhile, the company has no next generation exposure in the single aisle engine market as it was bought out of the IAE consortium providing the previous generation IAE V2500 turbofan and now only harvests the power-by-the-hour revenues for that but has no next generation in-service engine. So, for a big part of the future market, Rolls-Royce does not provide a solution. That could possibly change with the UltraFan, which should be a scalable power plant but that is really a power plant we would be seeing on new airplane developments of which none are announced at this point and none are expected to be announced in the years to come. So, a meaningful role is somewhat reserved for the mid-decade to end-decade timeframe and the company is currently already seeing that some airlines are not opting for the Airbus A350 powered by the Trent XWB due to durability concerns. A recent example is the consolidation order for the Airbus A350 signed with Emirates. The initial expectations were that the Airbus A350-1000 would also be ordered and the quantity would be at least three times the number of airplanes ordered now, but that didn’t happen due to durability concerns.

A Look At The Rolls-Royce Results

Rolls-Royce

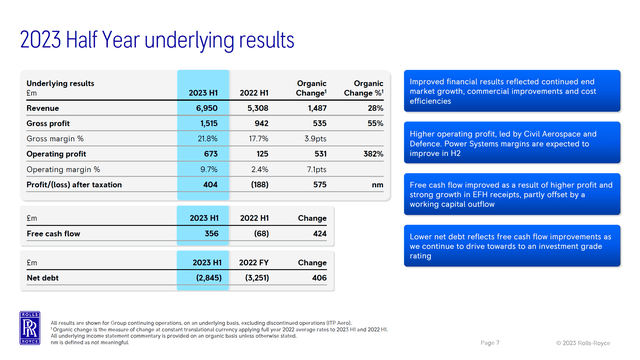

Rolls-Royce provides detailed financial information every six months contrary to the usual quarterly basis, so I will be analyzing the H1 2023 results. Those results show 28% growth in revenues and 55% growth in gross profit as well as 382% growth in operating profits.

The big driver were increased engine flying hours where large engine flying hours were 83% recovered leading to 38% growth in revenues driven by 58% growth in deliveries to OEMs and 30% growth in services revenues. Defence revenues increased 15% driven by 17% higher OEM sales and 13% higher services sales with a 33% increase in operating profits.

Power Systems sales increased 24% driven by 33% higher OEM sales and 10% higher services sales with operating profits increasing 5% and New Market accounted for 0.01% of the revenues and it is currently a loss-making business as this segment focuses heavily on development for future applications.

Overall, the business is performing well I would say and there is significant upside to recovery as there still is 17% in engine hours to be recovered compared to 2019 on top of which higher production rates should provide positive layering to the top line and eventually the bottom line with long-term returns.

Can Rolls-Royce Stock Fly Even Higher?

The Aerospace Forum

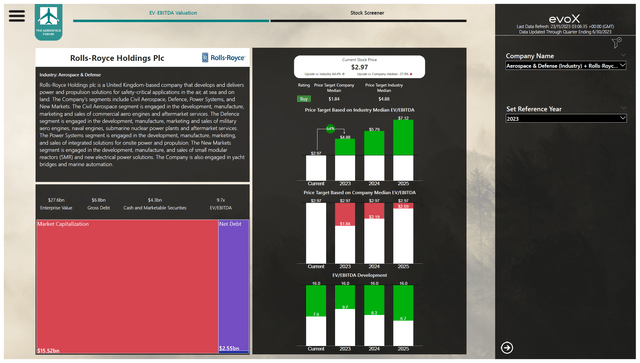

Rolls-Royce stock has gained almost 190% over the past 12 months, which begs the question whether the company can fly even higher and I would say it can. The company is significantly overvalued against its median EV/EBITDA, but I would not say that a company median of 6x is justified as this presents a 62.5% discount to peers. If Rolls Royce were to trade in line with peers, the upside would be significant, namely 64% with a $4.88 price target. I would not want to make the case for a direct industry valuation to be representative of the upside, but I would think that valuation in between would be justified which would bring my price target to $3.35 providing 15% upside which is slightly higher than the average target set by Wall Street analysts.

Conclusion: Rolls-Royce Can Fly Even Higher

In the near-term, I believe Rolls-Royce has a lot of growth drivers in the sense that engine flight hours are only 83% recovered, while over the longer term, the company has significant opportunities to increase commercial aerospace revenues on the back of Airbus A350 and Airbus A330neo sales. Simultaneously, I also do have to note that the company has little exposure to new engine programs for single aisle airplanes which provides some pressure as IAE V2500 airplanes will over time see reduced value for the Rolls-Royce as airplanes powered by those propulsion systems are being replaced by new technology airplanes to which Rolls-Royce has no exposure. However, the current shortage of airplane does provide some support to the older generation airplanes to which Rolls-Royce does have exposure. Besides that I also see positive demand trends in New Market which could increase demand for electrical solutions as well small nuclear reactors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here