Post the approval of the merger between SPAC Digital World Acquisition Corp. and Trump Media and Technology Group Corp. (NASDAQ:DJT), shares of DJT (formerly DWAC) have rocketed. This rally came on the back of a long merger process and reflects the excitement of the company’s investor base to have access to an ownership share of Truth Social, the flagship product of DJT.

However, on all conventional metrics, the company’s stock has been trading at stratospheric valuation levels for the past few months. Levels so high, that they are impossible to reconcile with the company fundamentals. My belief is that the stock is functioning in a manner that is much more akin to the “meme stocks” that were common in financial markets in late 2020, and which recently went through a resurgence, than it is to a stock trading on fundamentals. Due to this, even if Truth Social manages to find some success, it is in my view unreasonable to expect it to be able to support DJT’s current valuation and in the long run, DJT will likely go the way of other companies such as Quantumscape (QS) or GameStop (GME), which experienced massive declines after the companies started trading on valuations driven by underlying fundamentals.

Valuation

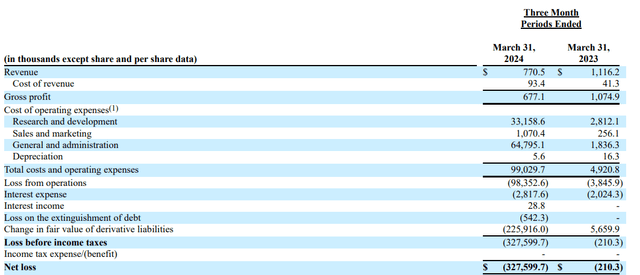

The argument for DJT being overvalued is straightforward. The company is loss making, reporting an operating loss of over $98 Million in Q1 of 2024, Furthermore, it only reported revenues of $770,000 in the same quarter, a decline year on year from the $1,116,000 generated in Q1 2023.

DJT 2024 Q1 earnings (SEC)

These meager sales are asked to support a monstrous $8 billion market cap, giving DJT a trailing TTM price to sales ratio of well over 1000x. It’s extremely rare for even ultra high growth companies to trade at these multiples, never mind DJT, which is posting declining revenue. Needless to say, it is borderline impossible for this situation to last. Take a much larger, more established player in the social media market for comparison: Snapchat (SNAP). SNAP has about 1000x the annual revenue of DJT, but despite this, only has a market cap 3x that of DJT.

To make a generous estimate of the true value of DJT, we can perform a simple comparison to X (formerly Twitter), the market leader in the social media space which Truth Social is trying to compete in (microblogging). If we rely on Fidelity and take the valuation of their stake in X, X is likely worth around $12 Billion, 50% more than the current valuation of DJT.

If DJT is successful in becoming a market leader in the microblogging niche of the social media industry, a difficult feat which I will generously assign a 10% probability of succeeding at, the company will probably be worth slightly less than X is currently (since X, Threads etc. won’t simply disappear as competitors). In this scenario, DJT probably commands a valuation of around $8 Billion.

If DJT is unsuccessful in becoming a market leader, due to network effects which cause social media to be a winner-take-all industry, the company is probably only worth $0.5 Billion. I’ll assign a 90% probability to this.

Taking the probability weighted sum, we get $1.25 Billion, applying a discount rate to this, since it probably takes at least 2 to 3 years to become the market leading company in the niche, fair value is likely around $0.8 Billion in an analysis which makes assumptions about the future of Truth Social, which are in all likelihood probably too positive.

Since this simple analysis of DJT’s valuation is quite conclusive, I’ll avoid going further into the ways in which the valuation doesn’t make sense, and instead attempt to answer the question: If fundamentals aren’t driving the price, then what is?

Factors Determining The Stock Price

In my view, the factors influencing the price of DJT are 3 fold:

- A portion of firm Trump Supporters, who view buying stock in DJT as a method of supporting Trump both financially and as a show of moral support.

- Meme stock like speculation due to the stock’s volatility and mainstream interest, as a result of being associated with such a public figure.

- The possibility that if Trump were to win re-election, presidential communications would be conducted through Truth Social, leading to a mass influx of users and a significant improvement in the company’s financial situation.

Whilst factor 1 is currently quite a relevant factor to analyze for anyone looking to trade DJT speculatively in the short term, over time, interest in buying this stock simply for support will likely fizzle out, in 5 years’ time it’s difficult to conceive of this group of investors still exerting significant buying pressure, when it’s not likely that Trump will even have major role in US politics by then (having either already served his 2nd term in office, or having suffered a second election defeat).

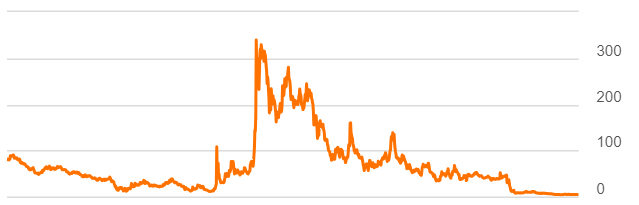

Factor 2 can again drive the price in the short term, but ultimately, nearly every meme stock’s hype eventually died down, and market forces pulled prices back down to earth, as was the case with AMC, for example:

AMC Stock Price (Seeking Alpha)

Factor 3 is more interesting, as it does present a long term threat to a DJT short thesis. However, Trump winning re-election is only one of the number of things which have to go right for Truth Social to gain a market-leading position in the microblogging space. Adoption from mainstream celebrities and advertisers would also be necessary and is a massive hurdle to overcome.

The interplay between these three factors will likely drive the price of DJT in the short to medium term. They may even lead to some interesting and unexpected outcomes. For example, if Trump were to lose the election, Factor 3 (The possibility of Trump winning re-election) would be dead in the water. You might expect a decline in price as a result of this, but it’s also possible that the stock would rally in the short term due to Factor 1 (Trump supporters seeking to show moral support for Trump after a loss).

Overall however, the effects of Trump voters buying shares to show support, as well as meme-stock like buying can be expected to wane and disappear within the next 5 years, leaving only company fundamentals to support the valuation – something, which as outlined in the previous section would likely lead to a large decline in share price.

Conclusion

Given the points made above, my expectation is for shares in DJT to be trading significantly lower than they are today in a few years time. The path which the share price will take to get there might however, involve many large rallies along the way, influenced by election and court case outcomes, as well as the future popularity of meme stocks in the market.

It’s not clear exactly how investors can take advantage of this. However, since DJT has an extremely high borrowing rate for short selling due to high demand, the stock also has a distorted options market, with put premiums so high, that only small profits can be made from large drops in stock price.

It thus may be prudent for investors to wait for more preferable options prices or borrowing fees before acting on DJT’s short thesis. Furthermore, the likelihood of large rallies along the way must be considered, when deciding on position sizing and how best to profit from a decline in the stock.

Read the full article here