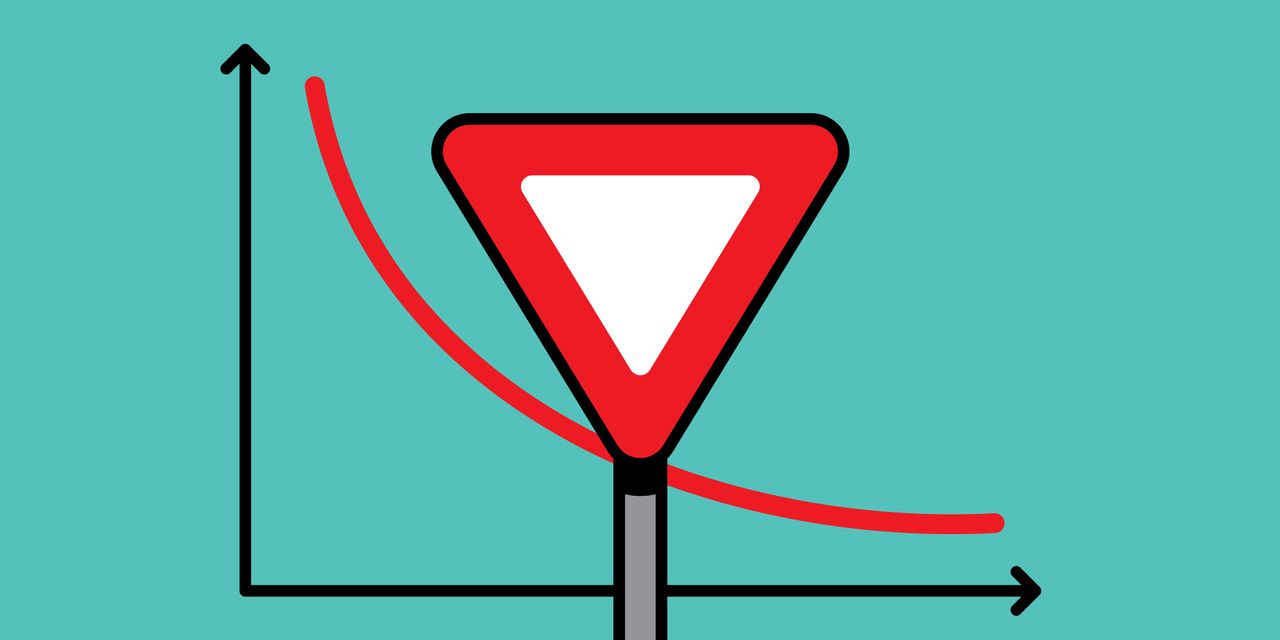

The yield curve is signaling a recession is coming, even as investors mostly shrug. For nearly a year, the chart plotting interest rates on U.S. Treasuries of different maturities has been downward sloping, meaning yields on longer-term debt are lower than on shorter-term securities: an “inverted” yield curve. Longer-term rates are normally higher because the chance of inflation and rate uncertainty rises with time; bond investors tend to seek higher yields to lend for longer.

An inverted yield curve can signal that investors expect higher rates or economic risk in the near term. An inverted curve has preceded every U.S. recession since the 1950s.

The yield on the two-year Treasury note is more than a percentage point higher than on the 10-year note, the largest gap since Silicon Valley Bank failed in March. An inversion this big hasn’t happened since the high inflation, rising rates, and recessions of the 1970s and ’80s. Dow Jones Market Data says inversions of two-year and 10-year yields have preceded recessions by as little as seven months or as much as two years, so a slump could be coming soon. A New York Fed recession model, using the three-month/10-year spread, spits out a 71% likelihood of a recession in the next 12 months.

But an inverted yield curve doesn’t say anything about the severity of a coming recession. The stock market’s resilience could be due to expectations of a shallow recession. The worst of the banking mini-crisis appears past, and there aren’t signs of an asset bubble or a credit crunch. Investors seem to believe inflation will continue to fall and labor markets will be resilient. “In our view, equity market investors are largely ‘looking through’ this classic recession signal,” writes Wolfe Research’s Chris Senyek.

Next Week

Monday 7/3

The Nasdaq and New York Stock Exchange have shortened regular trading hours, ending at 1 p.m.

The Census Bureau reports construction spending data for May. Consensus estimate is for spending to rise 0.4% month over month to a seasonally adjusted annual rate of $1.92 trillion.

The Institute for Supply Management releases its Manufacturing Purchasing Managers’ Index for June. Economists forecast a 47 reading, roughly even with the May data. The index has had seven straight readings below 50, indicating the U.S. is in a manufacturing recession. But continued strength in the services sector has lifted the overall economy up.

Tuesday 7/4

Equity and fixed-income markets are closed in observance of Independence Day.

The Reserve Bank of Australia announces its monetary-policy decision. Traders are pricing in a 25% chance that the RBA raises its key short-term interest rate by a quarter of a percentage point, to 4.35%. The central bank has raised rates 10 times since April 2022 for a total increase of four percentage points. With regional neighbor New Zealand having entered a recession, Australia’s chances of dodging its second recession since 1991 are 50/50, according to

Commonwealth Bank of Australia,

the nation’s largest lender.

Wednesday 7/5

The Federal Open Market Committee releases the minutes of its mid-June monetary-policy meeting.

Thursday 7/6

ADP releases its National Employment Report for June. Economists see a gain of 250,000 private-sector jobs, following a 278,000 increase in May. The leisure and hospitality sector continues to lead gains while manufacturing and finance shed workers in May.

The Bureau of Labor Statistics releases the Job Openings and Labor Turnover Survey. The consensus call is for 9.9 million job openings on the last business day of May, slightly less than in April. Despite falling by nearly two million from the peak of 12 million in March 2022, job openings remain historically elevated. There are currently 1.65 job openings for every unemployed person, and Federal Reserve Chairman Jerome Powell has stressed that he would like to see that ratio approaching 1:1.

The ISM releases its Services

PMI

for June. Expectations are for a 50.8 reading, a tick higher than the May figure. The index has had only one reading below the expansionary level of 50 in the past three years.

Friday 7/7

The BLS releases the jobs report for June. The consensus estimate is for the economy to add 212,500 nonfarm payrolls, after a 339,000 increase in May. The unemployment rate is seen remaining unchanged at a historically low 3.7%. Average hourly earnings are expected to rise 0.3% month over month, matching the May data. Jobs growth has surprised to the upside nearly every month in the past year, sometimes by more than double estimates, as in January.

Write to Nicholas Jasinski at [email protected]

Read the full article here